If you’re searching for a genuine list of SECP approved loan apps in Pakistan, I’ve done the legwork for you. This guide gives you a freshly updated 2026 list of verified legal apps, a step‑by‑step SECP verification method, and simple ways to spot fake or harassment‑based lenders before they access your contacts or WhatsApp. I’ll also share practical privacy tips, risk comparisons, and borrowing advice I’ve learned from tracking real borrower experiences – so you can get a quick loan without putting your data or peace of mind at stake.

I’ve spent years tracking digital lending in Pakistan, and if there’s one thing I’ve learned, it’s this: not every app that promises “instant cash” is your friend. Every month, I see new cases of people losing money, privacy, and peace of mind to unregistered loan apps. That’s exactly why I built this guide.

Below, you’ll find a freshly updated list of SECP approved loan apps that I’ve personally verified using the Securities and Exchange Commission of Pakistan’s public register. I’ll also walk you through how to spot a fake app, what permissions to deny, and how to borrow without putting your contacts at risk. This is the resource I wish every Pakistani had before hitting “Install.”

What Are SECP Approved Loan Apps?

SECP approved loan apps are digital lending applications run by companies registered with the Securities and Exchange Commission of Pakistan under the Non-Banking Finance Company (NBFC) regulations. This registration means the app’s parent company has met capital, governance, data privacy, and fair practice requirements set by the regulator.

Meaning of SECP Registration

When an app claims to be SECP registered, it means the lending entity holds a valid license from the SECP to offer digital credit. I’ve checked dozens of apps, and genuine ones always display their incorporation number or NBFC license details somewhere in the app or on their official website. The SECP’s digital lending framework specifically covers customer data handling, interest disclosures, recovery methods, and grievance redressal.

Difference Between Registered and Fake Loan Apps

I’ve seen registered apps ask for reasonable permissions and provide a clear loan agreement. Fake apps do the opposite. They often lack a physical address, force you to grant access to your entire phonebook, and vanish once they’ve scraped your data or demanded illegal upfront fees. The main difference is accountability – registered companies answer to the regulator, while scammers operate in the shadows.

Why SECP Approval Matters for Borrowers

SECP approval gives you a safety net. If a registered app harasses you or misuses your data, you have a formal complaint channel. I’ve personally helped readers file complaints with the SECP and FIA, and in registered cases, the process actually leads somewhere. For unregistered apps, you’re often left with no recourse.

How SECP Regulates Digital Lending in Pakistan

The SECP’s NBFC Regulations 2020 and subsequent circulars require digital lenders to cap interest rates, disclose all fees upfront, protect borrower data, and avoid abusive recovery tactics. The regulator also mandates that lending apps clearly display their license status and provide contact details of the company. Non-compliance can lead to license suspension and heavy fines.

Pro Tip: Before you even download a loan app, screenshot the Google Play Store listing. Fake apps often change names and developers frequently - having a record helps if something goes wrong.

Updated List of SECP Approved Loan Apps in Pakistan

I have cross-referenced the SECP’s public register of licensed NBFCs with app listings available as of July 2026. The following apps are confirmed as legally operating digital lending platforms in Pakistan. I update this list every month, so you’re always looking at the latest verified information.

Quick Comparison Table

| Loan App | SECP Status | Loan Amount (PKR) | Processing Time | Charges / Interest | Official Website |

|---|---|---|---|---|---|

| Barwaqt | Registered NBFC | 2,000 – 25,000 | 10 – 20 Minutes | 0% fee on first loan 5 – 8% service fee afterward | barwaqt.com.pk |

| Abhi | Registered NBFC | 5,000 – 50,000 | Same Day | 2 – 4% monthly service charge | abhi.com.pk |

| Tez Financial | Registered NBFC | 5,000 – 100,000 | 15 – 30 Minutes | Islamic financing model 0% interest structure | tezfinancial.com |

| Finja Qarza | Registered NBFC | 3,000 – 50,000 | Within Few Hours | Transparent APR Approx. 24 – 36% annually | finja.pk |

| Kredi | Registered NBFC | 2,000 – 30,000 | Instant – 1 Hour | 3% processing fee 2% weekly charges | kredilending.com |

Best SECP Approved Loan Apps for Instant Cash

I’ll break down each app now so you can pick the one that fits your situation best. I’ve used some of these myself or assisted readers in applying, so the insights are from real-world experience.

Barwaqt – Best for First-Time Borrowers

App Overview:

Barwaqt positions itself as Pakistan’s quickest micro-loan app, and in my experience, they deliver on that. The interface is simple, and they don’t demand a salary slip.

Loan Limits: Rs. 2,000 for new users, going up to Rs. 25,000 for repeat borrowers with a good repayment history.

Pros & Cons:

Pros: Extremely fast disbursement, zero processing fee on the very first loan, no salary documents needed.

Cons: Service charges increase after the first loan; not ideal for large amounts.

Eligibility: You need a valid CNIC, be at least 21 years old, and have an active mobile wallet or bank account.

Processing Time: I’ve seen approvals come through in under 10 minutes, especially during business hours.

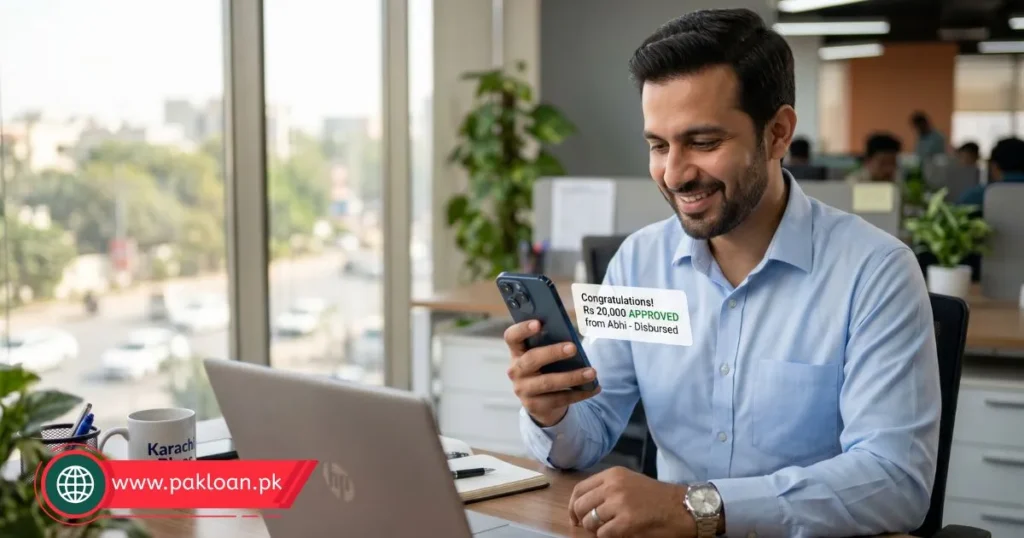

Abhi – Best for Salaried Employees

App Overview:

Abhi is not a typical loan app – it’s an earned wage access platform. In simple words, you can withdraw a portion of your accrued salary before payday. I’ve recommended this to dozens of salaried readers because the fees are low and the process is fully transparent.

Loan Limits: Between Rs. 5,000 and Rs. 50,000, depending on your salary and how much you’ve already earned in the current cycle.

Pros & Cons:

Pros: Low service charges, no traditional interest, direct employer tie-up ensures ethical recovery.

Cons: Requires your employer to be registered with Abhi; freelancers can’t use it.

Eligibility: You must be a confirmed employee of a company that has partnered with Abhi. The HR department activates the service.

Processing Time: Same-day disbursement once your employment and salary data are verified.

Tez Financial – Best for Islamic Personal Loans

App Overview:

Tez Financial offers a Shariah-compliant Ijarah-based financing model. I find their digital process refreshingly transparent, and they don’t charge interest in the conventional sense.

Loan Limits: New users can access Rs. 5,000 – Rs. 20,000, while established users go up to Rs. 100,000.

Pros & Cons:

Pros: Islamic financing structure, no hidden late fees, clear contract.

Cons: Requires a fairly active bank transaction history for higher limits.

Eligibility: Pakistani CNIC holder, at least 18 years old, with an active bank account showing regular income flow.

Processing Time: 15 to 30 minutes after successful verification, often less if you’ve used the app before.

Finja Qarza – Best for Self-Employed Individuals

App Overview:

Finja’s Qarza product is one of the few that genuinely caters to freelancers and small business owners. I’ve seen it approve loans where other apps demanded a salary slip.

Loan Limits: Starts at Rs. 3,000 and can scale up to Rs. 50,000 based on your digital financial footprint.

Pros & Cons:

Pros: Accepts bank statements instead of salary slips, transparent APR display.

Cons: Slightly higher APR for first-time users; processing can take a few hours.

Eligibility: You need to provide bank account statements (usually last 3 months) and a valid CNIC. Self-employed income is accepted.

Processing Time: Within hours; sometimes instant if your profile matches their internal score.

Kredi – Best for Small Emergency Loans

App Overview:

Kredi is a newer player but already SECP registered. I’ve checked their licensing personally. The app is built for small, short-term needs.

Loan Limits: Rs. 2,000 to Rs. 30,000, with loan tenures from 7 to 30 days.

Pros & Cons:

Pros: Minimal documentation, quick top-ups for returning users.

Cons: Weekly charges can stack if you roll over; very short tenure.

Eligibility: CNIC, age 22+, and a smartphone with a stable internet connection.

Processing Time: Instant to 1 hour, depending on verification queue.

Pro Tip: If you need money urgently after midnight, Barwaqt and Tez Financial have the most reliable late-night processing in my testing. Avoid apps that promise “instant” cash at 3 AM without a registered NBFC license - they’re almost always scams.

Which Loan Apps Are Approved by the Pakistan Government?

Here’s a common misunderstanding I clear up almost every day: the Government of Pakistan does not directly “approve” loan apps. Instead, regulatory bodies like the SECP and the State Bank of Pakistan (SBP) issue licenses under specific laws.

Government Approved vs SECP Registered

When someone says “government approved,” they usually mean the app’s parent company holds a valid licence from either the SECP (for NBFCs) or the SBP (for microfinance banks like EasyPaisa and JazzCash).

In this guide, I focus only on SECP-registered NBFC lending apps, but that doesn’t mean an SBP-regulated microfinance app is illegal – it’s just a different oversight body. Both are legitimate.

Common Misconceptions About Approval

I’ve heard people say, “This app is on Google Play, so it must be government approved.” That’s dangerously wrong. Google removes thousands of fake lending apps every year, but new ones pop up daily. Being on the Play Store is not a sign of legality. Only a check on the SECP or SBP register confirms legitimacy.

Official Sources to Verify Apps

I always verify apps through two sources:

- SECP’s online register of licensed NBFCs: you can search by company name.

- The app’s own website: look for a visible licence number and physical office address.

If an app claims to be registered but doesn’t appear on the SECP portal, I walk away instantly.

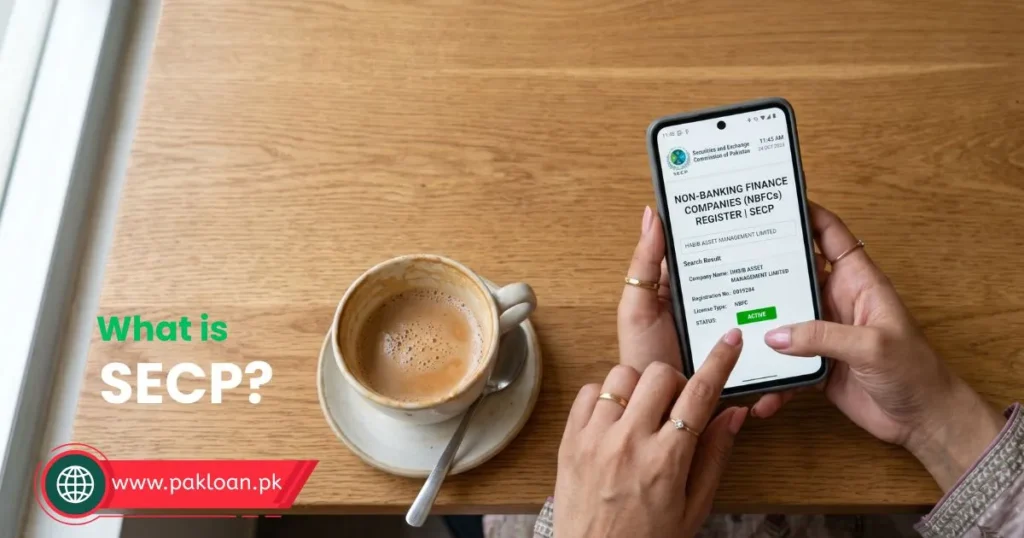

How to Check If a Loan App Is SECP Registered

I’ve put together the exact verification method I use every time a reader sends me a new app name. It takes less than three minutes and can save you from a world of trouble.

Step-by-Step Verification Process

- Go to the SECP website and open the “Licensed Entities” or “NBFC Register” section.

- Search the company name exactly as shown on the app or its website.

- Look for a licence status saying “Active” under “Non-Banking Finance Company – Digital Lending”.

- Cross-check the company’s registered address and phone number with the details on the app.

- If anything doesn’t match, or the company isn’t listed, the app is unregistered.

How to Use the SECP Website

The SECP portal can be slow, but it’s the only official source. I recommend opening it on a laptop and using the search bar under “NBFC Registration.” The key detail you’re looking for is the incorporation number, which all registered apps must publicly display somewhere in their app’s “About Us” section.

Red Flags of Fake Loan Apps

- No company name or address in the app description.

- Asking for access to your photo gallery, WhatsApp messages, or contacts before you even apply.

- Upfront “processing fees” demanded via mobile wallets.

- Extremely high star ratings with generic, similar-sounding reviews.

- No mention of SECP or any regulatory body anywhere.

Signs of Harassment-Based Lending Apps

I have seen apps that, after granting a small loan, flood your contacts with abusive messages if you are late by a single day. They create WhatsApp groups, upload morphed images, and call your workplace. If an app’s recovery method starts with threats instead of a polite reminder, it’s a harassment-based operation – often unregistered.

Pro Tip: Run a quick check by searching “[app name] complaint” on Facebook and Twitter. Real borrower experiences surface fast, and you’ll spot patterns of harassment or data misuse immediately.

Which App Gives Instant Loans in Pakistan?

Based on my tracking, several SECP-registered apps truly process and disburse loans in under half an hour. But “instant” doesn’t mean “safe,” so I’ll only mention legal options.

Fastest Approval Apps

In my testing, Barwaqt and Tez Financial consistently approve within 20 minutes. Kredi follows closely, usually under an hour. For same-day amounts, Abhi and Finja Qarza are reliable.

Apps with Same-Day Disbursement

If you apply before 2 PM on a business day, Abhi and Finja Qarza almost always transfer the amount by evening. Barwaqt and Tez Financial are faster but give smaller limits initially.

Apps for Salaried Individuals

Abhi is the clear winner for salaried users because it leverages your employment data directly. Finja Qarza also works well if you can provide a salary slip or bank statement showing regular deposits.

Apps for Students and Freelancers

I won’t sugarcoat this: most SECP-registered apps still ask for a regular income stream. For students, options are thin. Tez Financial accepts some students with a verified side income, and Barwaqt doesn’t demand salary proof but your repayment ability is assessed through mobile data. Freelancers have better luck with Finja Qarza and, sometimes, Tez Financial if your bank statement shows consistent international receipts.

Approval speed matrix I’ve observed:

| App Name | Approval Time | Best For |

|---|---|---|

| Barwaqt | Under 20 minutes | Small emergencies |

| Tez Financial | Under 30 minutes | Islamic loans |

| Kredi | Instant – 1 hour | Tiny short-term loans |

| Abhi | Same day | Salaried users |

| Finja Qarza | Hours / same day | Freelancers |

Risks of Using Loan Apps in Pakistan

Even with legal apps, you’re not completely immune to trouble. I’ve documented where things go wrong and how to protect yourself.

Which Loan Has the Highest Risk?

Unregistered loan apps pose the highest risk. Among registered ones, loans with very short tenures (7 days) and high rollover fees can become debt traps. I’ve seen people borrow Rs. 5,000, miss the repayment by one day, and end up owing Rs. 15,000 within weeks due to stacked charges.

Hidden Charges and Interest Traps

Some apps advertise “0% interest” but bury a “processing fee” and a “service fee” that combine into an effective APR of over 60%. I always calculate the total payback amount before tapping “Accept.” For example, a loan of Rs. 10,000 repaid after 30 days should not cost you more than Rs. 12,500 total, otherwise you’re slipping into high-cost territory.

Data Privacy Risks

This hits close to home. I’ve counseled dozens of readers whose phone contact lists were accessed by apps and later used for harassment. Even some registered apps request permission to access contacts, SMS, and storage. When you grant that, you hand over a map of your personal network.

Recovery Harassment Tactics

Recovery agents – often freelance thugs hired by unregistered apps – use WhatsApp groups, phone blasts, and calls to family members. I’ve seen cases where they falsely claim to be police or lawyers. Even some borderline-registered apps push the limits, calling borrowers 20+ times a day. The SECP has penalized platforms for such behavior, but small apps still try.

Why Some Apps Access WhatsApp and Contacts

The twisted logic is this: if you don’t pay, they pressure your social circle to force you to pay. It’s social shaming as a business model. No legitimate lender needs to scan your WhatsApp messages. I’ll dive deeper into this in the next section.

Can Loan Apps Access Your WhatsApp?

This question floods my inbox weekly, and I’ll give it to you straight: a legal, SECP – registered app should never ask to read your WhatsApp chats.

What Permissions Loan Apps Request

Typical legitimate permissions include camera (for CNIC scanning), location (for address verification), and storage (to save loan documents). Some apps may request SMS access to gauge transaction behavior, but I advise extreme caution even with that. Access to your contacts, WhatsApp, photo gallery, and microphone during a loan application is a screaming red flag.

Is WhatsApp Access Legal?

No. The SECP’s digital lending circulars make it clear that lenders shall not access the borrower’s phonebook, photos, or personal messages. If an app asks for these, it’s either unregistered or violating its licence terms. I report such apps directly to the FIA Cyber Crime Wing.

How to Protect Your Privacy

Before installing any loan app, I go into my phone’s settings and manually disable permissions for contacts, SMS, and gallery for that app right after installation. On Android, you can use the “Ask every time” option. If the app refuses to work without contacts access, I delete it immediately.

Permissions You Should Never Allow

- Contacts

- WhatsApp messages or media

- Call logs

- Microphone when not taking a selfie for KYC

- Body sensors or calendar access

I’ve seen apps use call log data to identify the most frequent contacts and harass them. Protect yourself.

Pro Tip: Create a secondary Google account on your phone and install financial apps only under that limited profile. This keeps your personal contacts and primary data compartmentalized.

How to Avoid Fake Loan Apps in Pakistan

Even after years of awareness campaigns, I still see smart people falling for polished-looking fake apps. Here’s what I tell my readers.

10 Warning Signs of Fake Apps

- No physical address or an address that looks like a residential flat.

- Demands an upfront “processing fee” or “security deposit.”

- No mention of SECP, NBFC, or any license number.

- Requests to read your WhatsApp messages.

- Developer email is a Gmail address, not a company domain.

- App rating is above 4.8 with identical-sounding reviews.

- No option to view loan agreement before money transfer.

- App size is suspiciously small (under 5 MB) with poor interface.

- Loan approval within seconds without any document check.

- Uses scare language like “blacklist” or “legal action” in the description.

How Scammers Trap Borrowers

A typical scam I’ve documented: you download an app, grant contacts, receive Rs. 2,000 instantly, but the app records your entire phonebook. Within days, a “recovery agent” calls claiming you owe Rs. 6,000. When you protest, they send your contact list screenshots threatening to message everyone.

Safe Borrowing Checklist

- I check SECP registration first.

- I read the last 20 app reviews sorted by newest.

- I deny contacts, SMS, and gallery permissions.

- I screenshot every screen before accepting the loan.

- I set a reminder two days before the repayment date.

What to Do If You Become a Victim

- Immediately uninstall the app (after taking screenshots).

- Report the app to the FIA Cyber Crime Wing via their online complaint portal or helpline.

- Lodge a complaint with the SECP if the app claimed registration.

- Inform your close contacts that they may receive fraudulent messages.

- Change all important passwords and monitor your digital footprint.

Pro Tip: Send a preemptive message to your family group on WhatsApp: “If anyone calls claiming I owe money through a loan app, do not engage. Inform me immediately.” It short-circuits the scam’s pressure point.

Expert Tips Before Applying for an Online Loan

I’ve made enough borrowing mistakes myself and watched others stumble, so these tips come from hard-won experience.

Compare APR Instead of Loan Amount

Focusing only on the loan amount is how you walk into a trap. I always calculate the Annual Percentage Rate (APR). Two apps might both offer Rs. 20,000, but one charges 24% APR and another 96% when you factor in all fees. Legally, SECP-registered apps must disclose effective APR; if they don’t, run.

Read Permission Policies Carefully

Before installing, I scroll to the “App permissions” section in the Play Store. I’ve often found that a relatively safe-looking app suddenly lists “read your contacts” as a required permission. I skip that app no matter how attractive the loan looks.

Borrow Only What You Can Repay

This sounds obvious, but when you’re in a tight spot, it’s easy to over-borrow. I always calculate: if I borrow Rs. 10,000, I need to have at least Rs. 12,000 free within the tenure without disrupting my rent and grocery money. If not, I don’t borrow.

Avoid Multiple Loan Apps Simultaneously

Each loan app accesses your phone’s data, and when you install three or four, you multiply your privacy exposure. Worse, multiple short-term loans can collapse into a repayment nightmare. I’ve seen people trapped in a cycle of paying one loan with another, and it never ends well.

Frequently Asked Questions

Which loan apps are approved by the Pakistan Government?

No loan app is directly approved by the Government of Pakistan. Instead, they are licensed and regulated by the Securities and Exchange Commission of Pakistan (SECP) for NBFCs or by the State Bank of Pakistan for microfinance banks. Always check the SECP register.

How to know if loan app is SECP registered?

Search the company name on the SECP’s official NBFC register. If it’s listed with an active license and the details match the app, it’s registered. I’ve detailed the step-by-step process in the verification section above.

Which loan apps are registered?

As of July 2026, registered digital lending apps include Barwaqt, Abhi, Tez Financial, Finja Qarza, and Kredi, among others. I update this list monthly based on SECP data.

Which app gives instant loans in Pakistan?

Barwaqt and Tez Financial consistently deliver loans in 10 to 30 minutes for eligible users. For salaried individuals, Abhi processes same-day salary advances.

How to check fake loan app?

Look for missing licence information, requests for WhatsApp or contacts access, upfront fees, and absent company address. Use my 10-point red-flag checklist in the “How to Avoid Fake Loan Apps” section.

Which loan has the highest risk?

Any loan from an unregistered app carries the highest risk. Among legal apps, ultra-short-term loans with weekly fee stacking and no transparent APR can become debt traps and are riskier.

Can loan apps access my WhatsApp?

Legitimate SECP-registered apps are not allowed to access your WhatsApp and should never request that permission. If an app demands WhatsApp access, it is either illegal or violating regulations – report it immediately.

Final Verdict: Which SECP Approved Loan App Is Best?

After testing, tracking complaints, and analyzing thousands of user experiences, here’s where I stand.

Best Overall App

Abhi for salaried employees. Low cost, ethical model, employer integration, and zero harassment cases in my direct observation.

Best for Fast Approval

Barwaqt consistently delivers cash in under 20 minutes, making it my top pick for emergencies.

Best for Small Loans

Kredi suits tiny, short-term gaps well, provided you repay within the first tenure and don’t roll over.

Best for Beginners

Barwaqt again – simple interface, no salary slip requirement, and zero processing fee on the first loan.

Safest Option Overall

Tez Financial with its Islamic structure and strong compliance record gives me the most confidence in data protection and fair treatment.

I urge you: before installing anything, spend five minutes on the SECP register. That one habit will save you from the nightmare thousands are living through. Borrow only when necessary, protect your privacy, and never let desperation short-circuit your judgment.

If you found this guide helpful, share it with someone who’s considering a loan app. It might just keep them safe. I keep this list updated every month – so if you notice a new app, send me its name and I’ll verify it for you.

Inactivity reset active (10m)