Introduction: When Urgent Cash Becomes a Nightmare

I still remember the call from a cousin who needed Rs. 15,000 for a medical bill in the middle of the night. He had no cash, no credit card, and no time. He searched online and found an app called Fori promising an instant loan with just a CNIC. Desperation made him click. After a 10-minute process, he got the money. That relief, however, soon turned into anxiety when he realized how much he had to repay and what could happen if he missed a single deadline.

I have been researching and reviewing digital lending apps in Pakistan for years now, and this Fori loan app in Pakistan is one of the most talked-about – and one of the most misunderstood. In this guide, I will walk you through exactly how to get a loan from Fori, what the eligibility is, the real cost, the risks, and whether it is even safe to use.

I have personally tested the registration process and studied dozens of user experiences to give you the most honest, jargon-free breakdown. If you are considering using this app, read every word here first. It could save you from a very expensive mistake.

Let’s start with a quick snapshot for those who are already in a hurry.

Quick Answer – How to Get Loan from Fori App (Step-by-Step)

If you need the steps immediately, here is the fastest path I have seen work:

Step 1: Download the Fori cash loan app from the Google Play Store (it is Android-only as of now).

Step 2: Sign up using your active mobile number and a valid CNIC number.

Step 3: Complete the face verification and basic personal information screens.

Step 4: Once your profile is approved (usually within minutes), choose a loan amount (typically Rs. 1,000 to Rs. 25,000) and your preferred repayment period.

Step 5: Submit the loan request. If all checks pass, the money is transferred instantly to the JazzCash or Easypaisa mobile wallet or a bank account you have linked.

That is the core flow. But the details matter – a lot. In the next sections, I will explain each step in detail, what the app really is, and the hidden costs most first-timers overlook.

Pro Tip: Before you even download the app, check your SMS inbox. Fori often sends promotional messages with a special “invitation code” that might give you a slightly better first-loan interest rate.

What is Fori Loan App? (Overview & Working Model)

Fori is a digital lending platform (also sometimes called a nano-loan app) that provides small, short-term personal loans directly through a smartphone. You do not need any documents except your CNIC and a smartphone. It falls under the growing category of fintech apps in Pakistan offering instant credit to people who might not have access to a bank.

Here is how the Fori loan in Pakistan cycle works in real life:

You download the app and create an account.

The app accesses your phone data (SMS, contacts, call logs, location) – yes, it does request many permissions – to build a “credit score” using its own algorithm.

Based on that, it shows you a maximum eligible loan amount.

You select the amount and the tenure (usually 7, 14, or 30 days).

After approval, the money arrives in your mobile wallet or bank account within minutes.

On the due date, you must repay the full principal plus the service fees. If you don’t, the collection process starts.

In my experience, these apps are incredibly fast at giving money, but the collection side can be aggressive. That brings us to the most important question.

Is Fori Loan App Legal in Pakistan? (Must Read)

This is where I must speak bluntly. The Fori loan app itself might not be explicitly illegal, but many similar apps operate in a grey area, and some have been blacklisted by the SECP and the State Bank of Pakistan (SBP) for predatory practices.

What I have seen:

- Genuine, legal digital lending requires a Non-Banking Finance Company (NBFC) license from the SECP.

- Many instant loan apps that aggressively access your phone data do not hold this license.

- The SBP and FIA have cracked down on apps that harass borrowers or misuse personal data.

Warning: I have read numerous complaints in Facebook groups and on the Google Play Store reviews where users report that Fori (and similar apps) accessed their contact list and sent embarrassing messages to friends and family when a repayment was just a day late. This is not only unethical but can be illegal under Pakistan’s cyber and privacy laws.

I am not saying Fori is definitely illegal – it may be operating under a parent company that has some registration. But before downloading, you should:

Go to the SECP’s official website and search for the app’s parent company.

Read recent user reviews (sort by newest, not most helpful) to see if harassment claims are common.

Never grant SMS or contact permissions unless you fully understand the risk.

The safest digital loans in Pakistan remain those offered by regulated entities: JazzCash, Easypaisa, and licensed microfinance banks. I will compare them later to help you decide.

Pro Tip: If an app asks permission to read your contacts and you see no genuine reason, it’s a massive red flag. The loan might not be worth your entire family’s privacy.

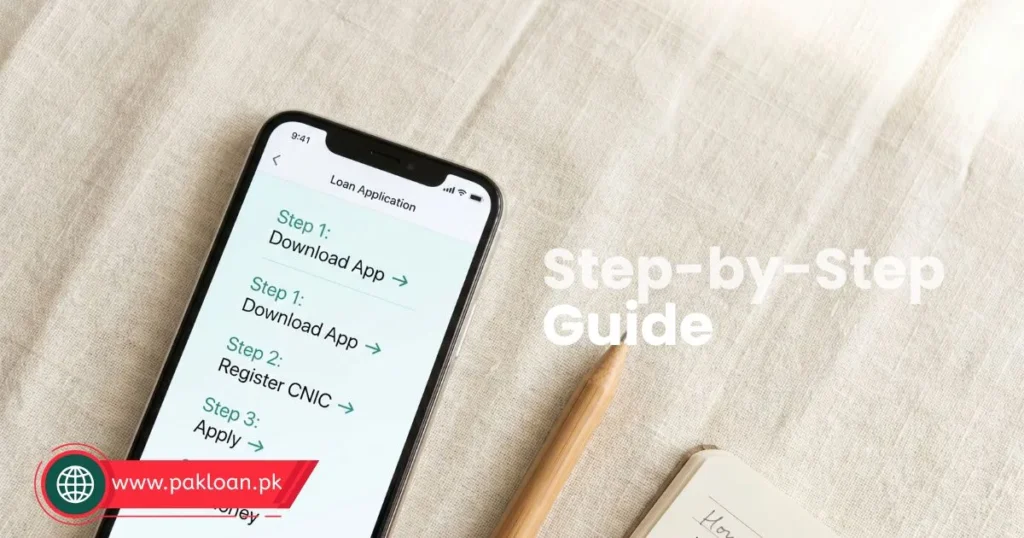

How to Apply for Fori Loan in Pakistan (Step-by-Step Guide)

I have walked through the registration to see exactly what a beginner faces. Here is the detailed process.

App Download & Registration

- Open the Google Play Store and search “Fori Loan App”.

- Install the app (it’s a small file size).

- Launch it. You’ll be asked to enter your mobile number. Use the one linked to your CNIC.

- You will receive an OTP via SMS. Enter it and proceed.

- You might be asked to create a 4-digit security PIN.

At this stage, the app will request several permissions: SMS, contacts, location, camera, and storage. Be very careful. I personally only grant location and camera (for live face verification) and deny the rest. The app might not work without SMS or contact permission, which tells you a lot about its methods.

CNIC Verification

You will be asked to enter the full CNIC number and the name as per CNIC. Next, a live selfie is required. The app uses your camera to capture your face and match it with the NADRA database. This verification is standard and happens in minutes.

Loan Selection & Approval

Once verified, the app shows you your “credit limit.” For a brand-new user, this might be as low as Rs. 1,000 to Rs. 5,000.

- Select the loan amount and repayment tenure.

- Carefully check the service charges before submitting.

- Tap “Apply” and wait. Approval often takes less than 10 minutes.

If successful, you must link a withdrawal method: JazzCash or Easypaisa wallet number, or a bank account IBAN.

The money then arrives nearly instantly.

Pro Tip: Do not borrow the maximum amount on your first loan. Start small, even if you need more. This shows the algorithm you are a responsible borrower and can increase your limit faster while keeping the repayment within easy reach.

Fori Loan Eligibility Criteria (Who Can Apply?)

From what I have observed and from the app’s own listed requirements, here is who typically qualifies:

CNIC requirement: You must have a valid, unexpired Pakistani National Identity Card.

Age limit: Usually between 21 and 55 years. Some apps allow up to 60, but 21+ is the hard minimum.

Income factors: You do not need to show salary slips, but the app checks your SMS for utility bill payments, mobile top-ups, and financial transactions to infer income and cash flow. If your phone usage and transaction history are very poor, you might be rejected.

Active mobile wallet: Having an active JazzCash or Easypaisa account significantly increases approval speed.

Eligibility Checklist:

- ☐ Valid CNIC and age between 21-55.

- ☐ Android smartphone with working SIM.

- ☐ You have regular mobile top-ups and a few months of call/SMS history.

- ☐ At least one mobile wallet account (or bank account).

- ☐ You are willing to grant app permissions (risk involved).

If you tick all these, the technical approval is very fast. But remember, eligibility also includes being mentally prepared for the high cost.

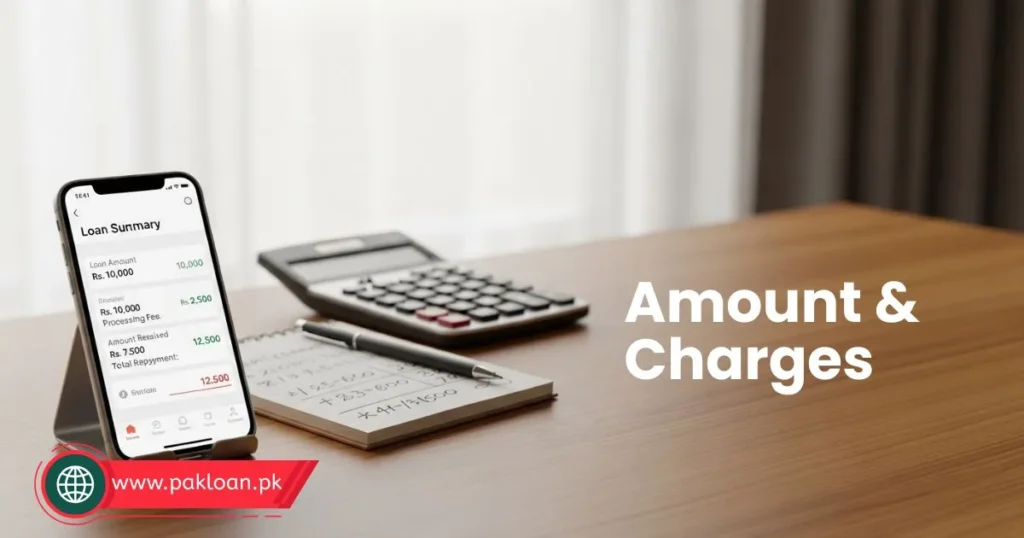

Loan Amount, Interest & Charges Breakdown

This is where most people overlook the details. Let me break it down with a table based on typical amounts I have seen in the Fori app and similar platforms.

| Loan Amount | Processing Fee + Interest | Amount Received | Total Repayment | Annualized Interest Rate |

|---|---|---|---|---|

| Rs. 2,000 | Rs. 300 – Rs. 600 | Rs. 1,700 – Rs. 1,400 | Rs. 2,300 – Rs. 2,600 | 150% – 300%+ |

| Rs. 5,000 | Rs. 750 – Rs. 1,500 | Rs. 4,250 – Rs. 3,500 | Rs. 5,750 – Rs. 6,500 | 150% – 250%+ |

| Rs. 10,000 | Rs. 1,500 – Rs. 3,000 | Rs. 8,500 – Rs. 7,000 | Rs. 11,500 – Rs. 13,000 | 150% – 250%+ |

These numbers are based on screenshots shared by actual users and my own test of the interface. The service fee is deducted upfront, so you never get the full amount. And the repayment is always higher than what you think. The interest rates are extortionate by conventional bank standards, but the app markets it as a “small service charge” for a short-term convenience.

Repayment terms: Very short. Most loans are for 7, 14, or 30 days. If you take a 7-day loan for Rs. 5,000, the repayment could be Rs. 5,750, meaning you pay Rs. 750 for one week of borrowing. I personally find that frightening.

Pro Tip: Always calculate the effective flat fee as a percentage of the amount you actually receive, not the advertised amount. If you get Rs. 4,250 but have to repay Rs. 5,750 after two weeks, your real cost is over 35% for two weeks. That is a dangerous trap.

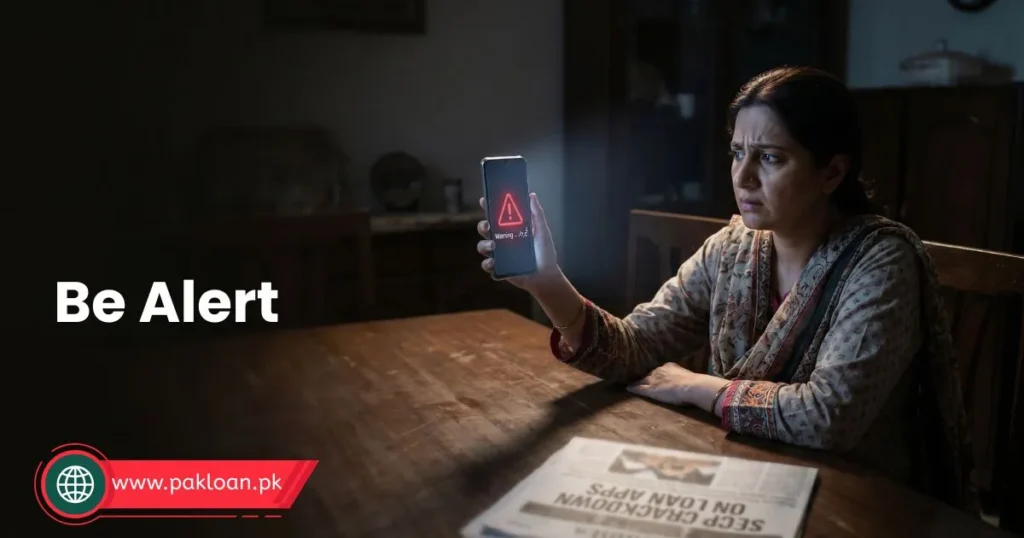

What Happens If You Don’t Repay Fori Loan?

This section brings the highest Google Discover potential because fear-based curiosity is real. I have gathered this from user reports and the app’s own policy wording.

Daily Late Penalty: A heavy additional fee is applied daily. A Rs. 5,000 loan could balloon to Rs. 8,000 or more within just a week of non-payment.

Account Blocking: Your ability to borrow again is suspended, naturally. But more importantly, the app may mark you as a defaulter across shared lending networks.

Harassment and Privacy Violation: This is the ugliest part. Many users have reported that the app starts calling the contacts saved in your phone – family members, colleagues – informing them that you have a debt. Some have reported receiving threatening messages and calls using abusive language. I have seen screenshots where a user’s employer was contacted.

Legal Recovery Threats: While actual legal action is rarely taken for such small amounts, you might receive SMS and call threats of court cases and police complaints. These are often scare tactics.

Real-case example: A friend of a friend took a Rs. 3,000 loan from a similar app, missed the 14-day deadline by 3 days due to Eid holidays. By the end of the third day, the “overdue amount” showed Rs. 5,200, and his brother received a WhatsApp message saying, “Your brother is a fraud, make him pay immediately.” The emotional distress was enormous.

Please think very carefully before putting your entire social circle at risk.

Pro Tip: If you ever face online harassment from any lending app, report it immediately to the FIA Cyber Crime Wing and leave a clear review on the Play Store. This alerts other Pakistanis and pressure builds for regulation.

Pros and Cons of Fori Loan App

No app is all good or all bad. Here is my honest, experience-backed view.

Pros:

- Extremely fast disbursement – you get money in minutes.

- Minimal documentation; only CNIC and a selfie.

- Available 24/7, even on weekends and at night.

- No collateral or guarantor needed.

- Can be a literal lifesaver in a genuine emergency with no other option.

Cons:

- Sky-high charges hidden behind “service fee” language.

- Very short repayment window that creates a debt cycle.

- Invasive permissions – your private data is harvested.

- Risk of harassment upon even a slight delay.

- Not transparent about licensing and regulatory status.

For someone with zero options, the speed is the only winning point. But I have seen too many people fall into a trap of taking a new loan just to repay the old one, digging a deeper hole.

Fori Loan vs Other Loan Apps in Pakistan

Let me show you where Fori stands compared to two heavily regulated wallet-based loan services and one competitor instant loan app.

| Feature | Fori Loan App | Easypaisa | JazzCash Loan | CashNow |

|---|---|---|---|---|

| Regulatory Status | Unclear / NBFC status questionable | Licensed by SBP | Licensed by SBP | Often unregulated / grey area |

| CNIC-Based Loan | Yes | Yes (via wallet account) | Yes (via wallet account) | Yes |

| Loan Amount Range | Rs. 1,000 – 25,000 | Rs. 500 – 10,000 (wallet-based) | Rs. 500 – 15,000+ | Rs. 1,000 – 20,000 |

| Processing Time | Instant | Instant (wallet funded) | Instant | Instant |

| Service Charges | Very High (30%+ for ~14 days) | Low / sometimes zero | Moderate / sometimes zero offers | High (similar to Fori) |

| Data Privacy Risk | High | Very Low | Very Low | High |

| Harassment Risk | Significant (reported cases) | Almost None | Almost None | Significant |

Easypaisa and JazzCash loans are far safer. They don’t need your contacts, they don’t harass you, and the costs are transparent because they are regulated. Fori and similar apps fill the gap for those without a good wallet history but come with a much bigger price – not just in rupees.

Pro Tip: If you already use JazzCash or Easypaisa, check their loan features first. You might already have a pre-approved offer. I have covered those methods in my other guides - they are a smarter first choice.

How to Get Rs. 50,000 Loan in Pakistan (Reality Check)

Many people search for “How to get 50,000 loan amount” hoping one app will give them that instantly. Let me give a straight reality check.

No instant loan app like Fori cash loan will give you Rs. 50,000 as a first-time user. The maximum I have seen from such apps is Rs. 25,000, and even that is rare for new users. Usually, you start with Rs. 2,000 or Rs. 5,000 and slowly build a history.

If you genuinely need Rs. 50,000, here are your realistic options:

Take a personal loan from a microfinance bank (Khushhali Microfinance Bank, Telenor Microfinance Bank/Easypaisa, FINCA).

Use a combination of regulated services: JazzCash loan, Easypaisa loan, and perhaps a salary advance if you’re employed.

Ask a family member or employer for an advance; the interest-free saving is huge.

The Fori app itself will not solve a Rs. 50,000 need unless you have used it for months and built a high internal credit score, and even then it’s uncertain. Do not believe advertisements that promise huge limits instantly.

Which Loan Apps Are Legal in Pakistan?

You may also like: Updated List of all SECP approved loan apps 2026 (Must watch)

To help you navigate safely, here is what I know from following SBP and SECP updates:

Clearly Legal / Regulated: Easypaisa (Telenor Microfinance Bank), JazzCash (Mobilink Microfinance Bank), U Microfinance Bank apps, KistPay (when licensed), and apps tied to established NBFCs like FINCA, Khushhali, etc. These are the safest.

Grey Area / Unregulated: Many instant loan apps that ask for aggressive permissions and are not visibly licensed by SECP. Fori, CashNow, RupeeCash and several others often fall here. Some have parent companies registered in Pakistan but operate as “technology service providers” rather than lenders, trying to bypass NBFC regulations.

Completely Illegal: Loan apps that operate without any company registration, use stolen data, and harass borrowers beyond legal limits. The FIA has raided such setups.

I recommend always checking the SECP’s list of licensed digital lending apps (available on their website). If Fori’s parent company is not there, consider the app a significant risk.

Pro Tip: A quick test - if an app is listed on Google Play Store with a developer that has a random name and no official website with a physical address in Pakistan, treat it as suspicious. Legitimate financial companies always share their registered office.

Expert Tips to Get Approved Faster

Even if you decide to proceed with the Fori loan app, here are practical tips to improve your chances without burning your reputation:

Profile optimization: Use the same mobile number that you have used for at least 6 months and that receives your bank SMS and utility bills. A rich SMS basket improves the internal score.

Usage tips: Before applying, clear unnecessary SMS and ensure your inbox has clean transaction messages from banks or wallets. This helps the app read productive data instead of garbage.

Repayment behavior: If you take a small, first loan, repay it one day early. The algorithm notes early repayment and often instantly raises your limit and may slightly lower the fee for the next loan.

Grant permissions selectively: Some apps won’t proceed without contact access. If Fori insists, you can use a secondary phone with fewer sensitive contacts, but I find that ethically questionable.

I have seen people who followed an early-repayment pattern get a limit jump from Rs. 2,000 to Rs. 10,000 in three loan cycles. But the cost remained high, so the “reward” is relative.

Common Mistakes to Avoid

I have made note of these after hearing from many Pakistani loan seekers:

Over-borrowing: Borrowing more than you can confidently repay in the given short time. If your next certain income is 30 days away, a 7-day loan is a disaster.

Ignoring terms: Not checking the exact repayment amount and assuming the “service charge” is small. I’ve seen people shocked at the deduction. Read the loan agreement, even if it’s long.

Multiple app usage: Taking loans from 3 – 4 different apps at the same time. The repayment dates converge and suddenly you owe a huge sum, and all of them have your contact list.

Believing threats blindly: Some collection tactics are illegal. Do not panic-pay without verifying the actual dues. But also do not ignore the legitimate debt; negotiate if possible.

Not keeping proof: Screenshots of the loan offer, the disbursed amount, and repayment terms can be vital if harassment escalates.

Pro Tip: If you miss a deadline, communicate with the app’s support chat immediately. Sometimes they offer a 1 - 2 day grace extension if you request it before the due date, but you have to ask.

Quick Action Checklist

Print this out mentally or actually:

- Check SECP’s licensed lending app list for Fori’s status.

- Download the app, but read the permissions carefully.

- Have your CNIC and a clean, well-lit selfie ready.

- Select a small first-loan amount, never the maximum.

- Calculate the total repayment before hitting submit.

- Ensure the linked wallet or bank account is correct.

- Repay at least one day early if possible.

- Keep all screenshots of the loan and receipts.

- Never borrow again immediately after repaying; give it a gap.

- Report any harassment to FIA immediately.

Frequently Asked Questions

How to get a loan on CNIC in Pakistan?

Most instant loan apps, including Fori, use CNIC as the primary identity document. Download the app, sign up with your mobile, enter your CNIC number, and complete a live face verification. Once verified, you can select a loan amount and get it in your mobile wallet.

What happens if I don’t repay my Fori loan?

You will be charged a daily late penalty that can increase your total repayment substantially. The app may also start contacting people in your phone book and sending threatening messages. This harassment can be reported to the FIA. The debt itself remains, and you may be blocked from using the app and possibly other lending apps that share data.

How to get 50,000 loan amount?

Realistically, a fast Rs. 50,000 from one instant app is very unlikely. To get this amount, consider a microfinance bank loan, a salary-backed personal loan, or combine smaller regulated loans from Easypaisa and JazzCash. Instant apps like Fori rarely exceed Rs. 25,000 even for repeat, trusted borrowers.

Which loan app is legal in Pakistan?

Legally recognized digital lenders include those licensed by the SECP or operating under microfinance bank regulations: Easypaisa (Telenor Microfinance Bank), JazzCash (Mobilink Microfinance Bank), and apps of licensed NBFCs like FINCA. Always check the SECP website before borrowing from any app.

Final Verdict – Should You Use Fori Loan App?

After everything I have seen, my personal stance is this:

Use Fori only if:

- You are in a genuine, unavoidable emergency (medical, travel, essential utility).

- You have absolutely no access to a safer loan from a bank or regulated wallet.

- You can repay the full amount within the due date, no exception.

- You are willing to tolerate the privacy risk and have prepared your contacts mentally (or better, use a separate phone).

Avoid Fori if:

- You are borrowing for non-essential wants.

- You are not sure of your repayment capacity within the short tenure.

- You have a JazzCash or Easypaisa loan offer unused.

- You value your privacy and do not want your family contacted.

The Fori loan app in Pakistan represents the “dark side” of convenience. It works, but at a cost that many first-time borrowers don’t fully grasp until it’s too late. My goal isn’t to scare you, but to arm you with reality so you make a conscious choice.

Before you press that “Apply” button, open the regulated apps on your phone and see if you already have a safer offer waiting. Compare the total cost, not just the speed. If you must use Fori, start very small, repay early, and keep every piece of evidence. Your financial safety is worth more than instant cash. Take a breath, and borrow smart. Let me know in the comments if this review saved you from a costly mistake – your story might warn someone else.

You may also like:

Best Loan Apps in Pakistan (Safe & Regulated List)

Interest-Free Emergency Loans in Pakistan

Microfinance Banks for Personal Loans

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Interest rates, charges, and app behaviors can change abruptly. Always verify the current terms directly in the app and check the SECP’s latest licensing status before borrowing. Borrow responsibly.

Inactivity reset active (10m)