Agriculture remains the backbone of Pakistan’s economy, contributing around 20% to GDP and employing nearly 40% of the workforce. However, small and medium-scale farmers often struggle to access affordable financing. This is where an agricultural loan in Pakistan becomes crucial—offering funds for seeds, fertilizers, machinery, and working capital.

In this post, we’ll explore the top 7 agricultural loan providers in Pakistan, comparing their features, interest rates, eligibility criteria, and application processes. By the end, you’ll have clear insights into which bank or institution best suits your needs.

You may also like: How to get Interest-FREE agriculture loan in Pakistan

Securing an agricultural loan in Pakistan is not just about getting money; it’s about choosing the right partner who understands rural credit challenges. From government-backed development banks to Shariah-compliant financiers, each lender has unique advantages. Let’s dive into detailed comparisons and help you make an informed decision.

Tip: Before applying for any agricultural loan in Pakistan, prepare a simple farm business plan that outlines your crop cycles, expected costs, and projected revenues. This will speed up the approval process.

Why an Agricultural Loans Matter in Pakistan?

Pakistan’s rural economy faces several hurdles: high input costs, unpredictable weather, and middlemen-driven supply chains that squeeze farmer margins. An agricultural loan in Pakistan provides timely access to funds for:

- Purchasing certified seeds, fertilizers, and pesticides

- Investing in drip-irrigation or solar-powered tube wells

- Procuring tractors, harvesters, and farm implements

- Covering day-to-day expenses such as labor and utilities.

Example: A wheat grower in Punjab may need to invest PKR 500,000 in quality seed and fertilizer two months before the harvest. Without financing, they rely on informal lenders charging up to 36% annual interest—eating into profits. In contrast, an agricultural loan in Pakistan from a reputable bank can offer rates as low as 6% per annum, allowing the farmer to reinvest savings into mechanization or crop diversification.

Tip: Track the State Bank of Pakistan’s policy rate announcements, as most commercial banks adjust their agricultural loan interest rates accordingly.

How We Chose the Top 7 Providers

We evaluated dozens of banks and microfinance institutions based on:

- Interest Rates & Profit Rates: Lower markup or profit rates help keep repayments manageable.

- Loan Limits & Tenure: Ability to fund smallholder farmers as well as larger operations.

- Collateral Requirements: Collateral-free or minimal collateral options reduce barriers for landless or marginal farmers.

- Geographic Coverage & Branch Network: Nationwide availability ensures rural farmers aren’t deprived of services.

- Value-Added Services: Technical guidance, training, and market linkages that complement financing.

You may also like: How to get small business loan in Pakistan FAST!

Our research relied on official bank websites, State Bank of Pakistan circulars, and recent press releases. We prioritized lenders that actively promote rural credit and have demonstrated commitment to agricultural development.

Tip: Often, specialized agricultural development banks offer collateral-free or interest-subsidized loans, while commercial banks provide more diversified products. Match the lender to your exact needs.

1. Zarai Taraqiati Bank Limited (ZTBL)

Overview:

Zarai Taraqiati Bank Limited (ZTBL) is Pakistan’s largest public-sector agricultural bank, with over 500 rural branches and specialization in farm finance. Founded in 1961 as ADBP, ZTBL offers a wide spectrum of agricultural loan in Pakistan products, from short-term crop loans to long-term farm development credit.

Key Products & Features

- Kisan Dost Production Loan: Short-term financing for inputs (seeds, fertilizers, pesticides) with a 3% rebate on timely repayment.

- Asan Qarza Scheme: Collateral-free Qard-e-Hasan (interest-free) loans up to PKR 100,000 for small farmers.

- Tractor & Mechanization Loans: Financing for tractors and machinery, with markup rates around 19.5% (rebate possible if repaid timely)

- Farm Development Loans: Long-term credit for construction of cold storages, processing units, and farm infrastructure.

Eligibility:

- Pakistani national with valid CNIC

- Minimum 5 acres of agricultural land (for mechanization loans)

- No prior default in the banking system (CIB clear)

- Completed application form and submit Fard/khatauni (land record).

Application Process:

- Online or Branch Visit: Complete ZTBL’s digital application or download the form

- Document Submission: CNIC copy, land record (Fard/khatauni), recent utility bill, and farm business plan.

- Verification & Disbursement: ZTBL officer conducts field verification. Upon approval, funds are released—typically within 2–4 weeks.

2. National Bank of Pakistan (NBP)

Overview:

NBP’s Kisan Dost and Kisan Taqat programs are designed to support both landholding and landless farmers. NBP remains one of the largest commercial banks active in rural credit, with designated agriculture branches nationwide.

Key Products & Features:

Kisan Dost:

- Loan Type: Short-term production financing (seed, fertilizer, labor)

- Interest Rate: Competitive markup (subject to SBP policy + spread)

- Collateral Options: Passbook, residential/commercial property, gold ornaments, or land record

- Tenure: Up to 3 years (revolving credit, renewable annually)

Kisan Taqat:

- Loan Type: Long-term project financing for dairy, poultry, fisheries, and value-addition units.

- Interest Rate: Slightly higher than Kisan Dost but subsidized for women borrowers.

- Collateral Options: Mortgage of land or property; gold ornaments accepted for smaller loans.

Eligibility:

- Valid CNIC and proof of residence

- Land record (Fard) for landholding farmers or witness/jep sheet for landless applicants

- Completed farm feasibility report (provided by NBP technical staff)

- No CIB default history

Application Process:

- Visit NBP Agriculture Branch: Obtain Kisan Dost application form.

- Submit Documents: CNIC, land record (if any), utility bill, and 2-page farm feasibility report.

- Technical Assessment: NBP’s agronomy team reviews farm operations and validates cost estimates.

- Disbursement: Upon approval, disbursed within 2–3 weeks.

Tip: Female farmers receive a 1% discount on markup rates under the Kisan Gold Loan.

3. Bank of Punjab (BOP)

Overview:

BOP’s Kissan Dost Production Loan and Farm Mechanization schemes cater to small and medium farmers, offering streamlined processes for crop inputs and equipment financing.

Key Products & Features:

Kissan Dost Production Loan:

- Loan Limit: Up to PKR 500,000 for crop-related inputs

- Interest Rate: SBP discount window rate + margin (approximately 7%–9% p.a.)

- Collateral: Land documents or acceptable third-party guarantees

- Tenure: Up to 12 months (aligned with crop cycles)

Kissan Farm Mechanization Loan:

- Loan Limit: Up to PKR 1,500,000 for tractors, combine harvesters, and allied machinery

- Interest Rate: 8%–12% (based on asset value and down payment)

- Collateral: Hypothecation of financed equipment plus land mortgage for higher amounts

- Tenure: 5–8 years (including grace period)

Eligibility:

- Valid CNIC and proof of residence

- Agricultural land proof (Fard/Khatauni) or CIB clearance for smaller loans

- Minimum education: primary level (for loan processing)

Application Process:

- Download Form

- Document Submission: CNIC, land record (if any), utility bill, latest bank statement (if existing business).

- Branch Verification: BOP officer verifies documents and may conduct a brief site visit.

- Disbursement: Funds credited to designated farm account within 10–15 working days.

4. Bank Al Habib

Overview:

Bank Al Habib offers multiple agriculture finance products under its “Kissan Revolution” banner, catering to crop production, mechanization, and value-chain financing.

Key Products & Features:

Kissan Revolving Credit Scheme:

- Purpose: Timely provision of crop inputs (seeds, fertilizers, pesticides)

- Credit Limit: Up to PKR 1,000,000 (renewable for 3 years with one-time documentation)

- Interest Rate: 9%–11% (subsidized by SBP; subject to revision)

- Collateral: Land record and warehouse receipt for stored produce (EWR)

Farm Production Financing Scheme:

- Purpose: Financing for value-addition (cold storage, processing units) and non-crop agri-businesses

- Credit Limit: Up to PKR 5,000,000

- Interest Rate: 10%–12% (linked to SBP policy rate)

- Collateral: Warehouse receipt, land mortgage, or hypothecation of equipment

Farm Mechanization Scheme:

- Purpose: Purchase of tractors, treaders, threshers, and allied machinery

- Credit Limit: Up to PKR 2,500,000

- Interest Rate: 8%–10% (depending on down payment)

- Collateral: Hypothecation of financed machinery plus land record for higher amounts

Eligibility:

- CNIC and valid land record (Fard/Khatauni) for crop-based loans

- Detailed equipment quotation for mechanization loans

- CIB report (no default)

Application Process:

- Online Inquiry: Submit details Online.

- Branch Visit: Present CNIC, land record, bank statements (if existing farmer).

- Technical Appraisal: Bank’s agri-finance team validates project feasibility.

- Disbursement: Typically within 2–4 weeks upon approval.

5. JS Bank

Overview:

JS Bank’s Agriculture Finance product is a specialized lending solution at a subsidized markup rate of 6% per annum, designed to support working capital and long-term investments in the farm sector.

Key Products & Features

Crop Production Finance:

- Loan Limit: Up to PKR 3,000,000 per farmer

- Interest Rate: Flat 6% p.a. (subject to SBP revision, benefit passed on)

- Tenure: Up to 12 months (aligned with crop season)

- Collateral: Land record or warehouse receipt.

Farm Machinery Finance:

- Loan Limit: Up to PKR 5,000,000

- Interest Rate: 6% p.a. (subject to SBP revision)

- Tenure: Up to 5 years (including a 6-month grace period)

- Collateral: Hypothecation of financed machinery; land mortgage for larger amounts

Livestock & Dairy Finance:

- Loan Limit: Up to PKR 1,000,000

- Interest Rate: 6% p.a.

- Tenure: Up to 3 years (complemented by technical guidance from JS Bank’s agri experts)

Eligibility:

- Valid CNIC and land record (where applicable)

- Completed application form with equipment quotations or projected livestock numbers

- CIB clearance (no defaults)

Application Process:

- Inquire Online: Visit jsbl.com/agriculture-finance

- Branch Submission: Submit CNIC, land record, and farm plan.

- Technical Assessment: JS Bank agronomists assess project viability.

- Disbursement: Funds credited to farm account within 10–15 working days.

6. Al Baraka Bank Pakistan

Overview:

Al Baraka Bank (Pakistan) Limited (ABPL) offers Shariah-compliant Zarai Finance products that cover working capital for crop inputs, farm development, and equipment financing albaraka.com.pk. Their profit-and-loss sharing model ensures ethical, interest-free financing.

Key Products & Features:

Al Baraka Khalyan Finance:

- Purpose: Purchase of inputs (seeds, fertilizers, pesticides)

- Credit Limit: Up to PKR 500,000

- Profit Rate: Based on commodity Murabaha cost + minimal spread (effectively 7%–9% p.a.)

- Tenure: Up to 12 months

- Collateral: Land record or warehouse receipt

Al Baraka Farm Development Finance:

- Purpose: Cold storage, silos, solar-powered tube wells, irrigation systems

- Credit Limit: Up to PKR 5,000,000

- Profit Rate: 8%–10% (Shariah-compliant)

- Tenure: Up to 5 years (including 6-month grace)

- Collateral: Hypothecation of financed assets and land record for larger amounts.

Al Baraka Tractor Financing:

- Purpose: Purchase of new/used tractors (locally manufactured)

- Credit Limit: Up to PKR 2,000,000

- Profit Rate: 9%–11% (declining balance method)

- Tenure: 5–8 years (including 1-year grace)

- Collateral: Hypothecation of the tractor; land record for down payment >20%

Eligibility:

- CNIC and valid land record (where applicable)

- Minimum of 5 acres for tractor financing

- Completed Al Baraka farm financing application form

- CIB clearance (no default)

Application Process:

- Inquiry: Contact branch or visit Al Barka Bank

- Document Submission: CNIC, land record, equipment quotation, and farm plan.

- Shariah Compliance Review: Al Baraka’s Shariah board reviews profit structure.

- Disbursement: Typically within 3 weeks after approval.

Tip: As a Shariah-compliant option, Al Baraka’s agricultural loan in Pakistan avoids riba. Combine it with government subsidies to minimize cost.

7. BankIslami Pakistan

Overview:

BankIslami provides Shariah-based financing to farmers across dairy, poultry, fisheries, and crop sectors. Their Agriculture Financing products emphasize ethical Islamically-compliant profit-and-loss sharing.

Key Products & Features

Dairy & Cattle Farming Finance:

- Credit Limit: Up to PKR 1,500,000 per farmer

- Profit Rate: 8%–10% (Shariah-compliant)

- Tenure: Up to 3 years (including 6-month grace)

- Collateral: Hypothecation of livestock or land record for larger amounts

Crop Production Finance:

- Credit Limit: Up to PKR 1,000,000

- Profit Rate: 7%–9% (declining balance)

- Tenure: Up to 12 months

- Collateral: Land record or warehouse receipt

Poultry & Fish Farming Finance:

- Credit Limit: Up to PKR 2,000,000

- Profit Rate: 9%–11% (Shariah-compliant)

- Tenure: Up to 2 years (including 3-month grace)

- Collateral: Hypothecation of assets; land record for high-value loans

Eligibility:

- Valid CNIC and proof of residence

- Farm feasibility report (prepared by BankIslami’s agronomy team)

- Land record (where applicable) or acceptable guarantor

- CIB clearance (no default).

Application Process:

- Branch Inquiry: Visit any BankIslami branch or contact the agri finance helpline.

- Submit Documents: CNIC, farm feasibility report, land record (if available).

- Shariah Screening: Profit structure reviewed for compliance.

- Disbursement: Funds credited within 15–20 working days on approval.

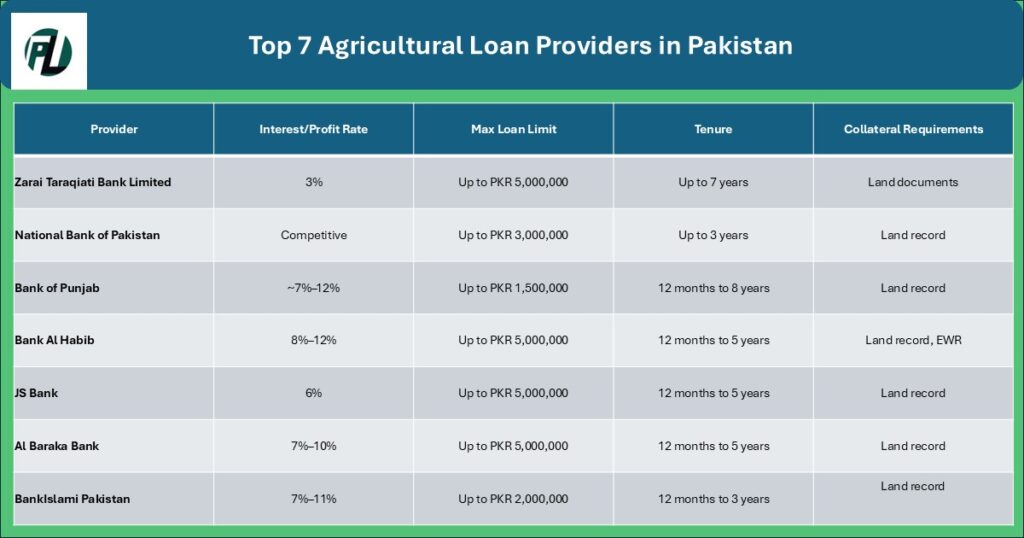

Comparative Table: Top 7 Agricultural Loan Providers

Deep Dive: Key Insights and Personal Experiences

ZTBL’s Rural Reach and Impact

ZTBL’s network of over 500 branches is unmatched. In district Chiniot, a small sugar-cane farmer, Ali Raza, took a PKR 300,000 agricultural loan in Pakistan under ZTBL’s Kisan Dost scheme last year. He used the funds to install drip irrigation. As a result, his water usage dropped by 40%, and his yield increased by 25%. ZTBL’s field officers provided on-site agronomic advice, ensuring Ali adopted best practices.

Tip: Always ask ZTBL field officers for free technical guidance—they often help with crop selection and pest management.

Leveraging NBP’s Kisan Taqat for Value Addition

Fatima Bibi, a dairy entrepreneur in Sahiwal, secured PKR 1 million under NBP’s Kisan Taqat scheme to build a small dairy processing unit. The competitive markup rate (just 8% p.a.) and doorstep technical guidance from NBP agronomy teams helped her produce packaged yogurt and paneer. Within six months, her monthly revenue doubled, allowing her to repay the loan ahead of schedule.

Tip: If you plan to diversify into value-addition (e.g., milk processing), prepare a three-page project report and request NBP’s technical team to review it before applying.

BOP’s Machinery Loans Amplify Productivity

In Faisalabad, Abdul Wahab used BOP’s Farm Mechanization Loan (PKR 1.2 million) to purchase a second-hand combine harvester. Even though he paid a 20% down payment, the 8% interest rate and 5-year tenure made repayments feasible. The combined machine reduced his harvesting time from two weeks to three days, and he now sub-lets the harvester to neighboring farms—generating an extra PKR 200,000 annually.

Tip: When acquiring used machinery, verify its condition with a trusted mechanic. BOP may finance up to 80% of the asset’s value but will require proof of inspection.

Shariah-Compliant Options: Al Baraka & BankIslami

For farmers preferring interest-free or profit-and-loss sharing models, Shariah-compliant lenders are ideal. Last winter, Mohsin Ahmed, a poultry farmer near Multan, borrowed PKR 800,000 from Al Baraka’s Farm Development Finance to build a small poultry shed. The 8.5% profit rate (declining balance) was acceptable because he valued the ethical financing structure and avoided riba.

BankIslami’s Dairy Farming Finance (PKR 500,000 loan at 9% p.a.) also helped rural families in Khyber Pakhtunkhwa expand their cattle herds (albaraka.com.pk, bankislami.com.pk).

Tip: If you choose Shariah-compliant financing, compare the total cost of financing (profit + fees) with conventional loans. Sometimes, a slightly higher profit rate still offers better flexibility and peace of mind.

How to Choose the Right Agricultural Loan Provider

1. Identify Your Financing Needs:

- Working Capital (Crop Inputs): Short-term (12 months) loans.

- Machinery & Equipment: Medium-term (3–5 years) loans.

- Value Addition (Processing Units): Long-term (5–7 years) loans.

2. Compare Interest/Profit Rates:

- If you need short-term financing, JS Bank’s 6% flat rate is very competitive.

- For ethical, interest-free options, consider ZTBL’s Qard-e-Hasan or Al Baraka’s Shariah model.

3. Assess Collateral Requirements:

- Landholding farmers with clear Fard/Khatauni benefit from lower rates at ZTBL or NBP.

- Landless farmers can explore Akhuwat Foundation (offering small, interest-free loans) or NBP’s Kisan Dost, which accepts guarantors and passbooks.

4. Evaluate Branch Access & Support Services:

- ZTBL’s extensive rural network provides on-site technical guidance.

- Bank Al Habib’s agronomy team offers feasibility studies for value-addition projects.

5. Check Application Turnaround Time:

- JS Bank and BankIslami often disburse within 10–15 working days.

- Government-backed schemes (ZTBL, NBP) may take 2–4 weeks due to field verification.

6. Leverage Subsidies & Government Programs:

- Under the 2024–25 Federal Budget, PKR 2,250 billion was allocated for agriculture credit, including PKR 10 billion for PM Youth Business & Agriculture Loans.

- Check if your lender participates in Ehsaas Kissan or Kamyaab Kisan programs for discounted rates or partial guarantees.

Tip: Always ask your bank officer if there are ongoing seasonal subsidy programs (e.g., fertilizer subsidy during plowing season) to reduce overall costs.

Frequently Asked Questions (FAQs)

What is agricultural finance?

Agricultural finance refers to specialized credit and banking services tailored to the needs of farmers and agribusinesses. It covers:

1. Short-term Loans: For crop inputs (seeds, fertilizers, pesticides) and working capital.

2. Medium-term Loans: For machinery, tractors, and equipment.

3. Long-term Loans: For farm infrastructure—cold storages, processing units, greenhouses.

4. Value-Chain Financing: Loans for storage, transportation, and marketing of agricultural produce.

Agricultural finance enables farmers to smooth cash flows, invest in productivity-enhancing technologies, and scale operations without resorting to informal, high-interest lenders.

Which bank is best for an agriculture loan in Pakistan?

There’s no one-size-fits-all answer; the “best” bank depends on your specific needs:

1. For Lowest Interest Rates (Short-Term): JS Bank at 6% p.a., ideal for working capital (jsbl.com).

2. For Collateral-Free Options: ZTBL’s Asan Qarza (interest-free up to PKR 100,000) and Akhuwat Foundation (Qarz-e-Hasan up to PKR 80,000).

3. For Value-Addition & Technical Support: NBP’s Kisan Taqat (comprehensive agronomy guidance) and Bank Al Habib’s detailed feasibility studies.

4. For Shariah-Compliant Financing: Al Baraka Bank and BankIslami offer profit-and-loss sharing models that avoid riba.

Consider branch proximity, turnaround time, and additional services (e.g., free training, market linkages) when choosing.

How much loan can I get on agricultural land in Pakistan?

Loan amounts vary widely based on the lender and purpose:

Short-Term Crop Loans: Typically range from PKR 50,000 to PKR 500,000 (e.g., ZTBL’s Kisan Dost, NBP’s Kisan Dost).

Machinery & Equipment Loans: Can go up to PKR 5,000,000 (e.g., ZTBL farm development, Bank Al Habib, JS Bank)

Value-Addition & Infrastructure Loans: Some banks (Bank Al Habib, ZTBL) offer up to PKR 10,000,000 for cold storages and processing units.

Prime Minister Youth Business & Agriculture Loans: Up to PKR 5,000,000 for young farmers (age 21–45) under PMYB&ALS 2025, interest-free for qualifying applicants.

Ultimately, your loan limit depends on collateral, project feasibility, and the specific scheme you choose.

Conclusion:

Access to an agricultural loan in Pakistan can transform a smallholder’s livelihood—enabling investment in high-yield seeds, modern equipment, and value-addition units that boost income and resilience. The top 7 agricultural loan providers discussed above each bring unique strengths:

- ZTBL: Nationwide presence, specialized agri-loans, and interest-free options for small farmers.

- NBP: Comprehensive Kisan Dost & Taqat programs with technical guidance.

- BOP: Flexible machinery financing and production loans aligned with crop cycles.

- Bank Al Habib: Diverse credit products from revolving credit to value-chain financing.

- JS Bank: Highly subsidized 6% markup rate, ideal for working capital.

- Al Baraka: Shariah-compliant profit-and-loss sharing model for ethical financing.

- BankIslami: Shariah-based dairy, poultry, and fisheries financing with professional support.

Evaluate each based on interest rates, collateral requirements, loan limits, and additional support services. Gather your CNIC, land record (if any), and a basic farm business plan before applying. With the right agricultural loan in Pakistan, you can boost your farm productivity, diversify income sources, and contribute to national food security. Good luck on your agricultural financing journey!

Inactivity reset active (10m)

1 thought on “Top 7 Banks Offering Agricultural Loan in Pakistan”