Introduction

kiaI still remember the conversation that inspired me to write this guide. A young couple – let’s call them Ayesha and Fahad – sat across from me in my office in Lahore, visibly overwhelmed. They had been saving for years, dreaming of owning their first home, but every time they encountered the word “mortgage,” their eyes glazed over. “We just want a simple explanation,” Ayesha said. “No jargon. No complicated terms. Just tell us – what is a mortgage in plain Urdu-English mix we can understand?”

What struck me most wasn’t their confusion. It was how avoidable that confusion was. In my 12 years of helping families navigate home financing across Pakistan, I have seen too many first-time buyers sign papers they didn’t fully understand, commit to terms that cost them lakhs of rupees unnecessarily, or worse – walk away from homeownership entirely because the process felt intimidating.

Here is the reality: a mortgage isn’t complicated. The industry has just made it sound that way. This guide will strip away the confusion, explain exactly how mortgages work in language any beginner can understand, and give you the knowledge to walk into any bank or lender with confidence.

By the time you finish reading, you will understand what a mortgage is, how payments work, what types exist (including Pakistan-specific Islamic options), what mistakes to avoid, and how to qualify – whether you are in Karachi, Islamabad, Multan, or anywhere else in Pakistan.

What Is a Mortgage in Simple Words?

When someone asks me to explain a mortgage in one sentence, here is what I tell them:

Simple Definition of a Mortgage

A mortgage is a loan that lets you buy a house now and pay for it over time – with the house itself serving as a guarantee to the lender.

Example: How a Mortgage Works with Real Numbers

Think of it like this: you want to buy a house worth PKR 1 crore (approximately Rs. 100,000), but you only have PKR 20 lakh in savings. A bank or financial institution lends you the remaining PKR 80 lakh. In exchange, you agree to pay back that loan in monthly installments over a set period, usually 15 to 25 years. If you stop paying, the lender has the legal right to take the property and sell it to recover their money.

How a Mortgage Loan Works – The Core Idea

Let me break this down into the simplest possible terms.

Two Parties in a Mortgage: Borrower and Lender

A mortgage involves two parties: you (the borrower or “mortgagor”) and the financial institution (the lender or “mortgagee”). The lender provides you with money to purchase real estate. You agree to repay that money, plus interest, in regular monthly payments.

Why a Mortgage Is Different from Other Loans

What makes a mortgage different from, say, a personal loan or a credit card? Two things:

It is secured by property. The house you buy serves as collateral. This security gives lenders confidence to offer larger amounts and longer repayment periods than they would for unsecured loans.

It is long-term. Most mortgage loans stretch across 15, 20, or even 30 years. This extended timeline keeps monthly payments manageable.

Pro Tip: When you hear the word "mortgage," mentally translate it to "house loan with a repayment plan." Understanding this core concept removes about 80% of the confusion most beginners face.

Who Owns the House During Repayment?

This is one of the most common questions I get, and it causes unnecessary anxiety.

Here is the truth: you own the house from day one. Your name goes on the title deed. You can live in it, renovate it, and call it home. The lender, however, places a “lien” on the property – a legal claim that says, “If you default on the loan, we have the right to take possession”.

In Pakistan, this arrangement works through what is called mortgage registration with the relevant land authority. The property is registered in your name, but the lender’s interest is also recorded. Once you make your final payment, the lien is removed, and you own the property outright – free and clear.

Four Core Mortgage Terms Every Beginner Must Know

| Term | What It Means | Simple Example |

|---|---|---|

| Principal | The original amount you borrow from the lender to purchase the property. | If you borrow PKR 80 lakh, that amount is your principal. |

| Interest / Markup | The cost charged by the lender for lending you money. | At 5% yearly markup on PKR 80 lakh, you pay around PKR 4 lakh per year initially. |

| Term / Tenor | The total length of time you have to repay the mortgage. | A 20-year mortgage term is common in Pakistan under government-backed schemes. |

| Monthly Installment | The fixed payment you make every month toward the mortgage. | Your installment includes both principal repayment + interest/markup. |

Quick Definition Box: What a Mortgage Is

| Question | Answer |

|---|---|

| What is a mortgage in simple words? | A mortgage is a loan used to buy property, repaid over time, with the property itself serving as security for the lender. |

| Who lends the money? | A bank, Islamic bank, microfinance bank, or housing finance company usually provides the mortgage. |

| Who owns the house during the loan? | You own the house, but the lender holds a legal claim (lien) and can act if you default. |

| How long do you pay? | Mortgage repayment is typically 15–25 years in Pakistan, and up to 30 years in some markets. |

| What happens if you stop paying? | The lender may seize and sell the property (foreclosure) to recover the outstanding loan. |

A Simple Example With Numbers

Let me give you a concrete example that makes the concept real.

Imagine you find a house in a Lahore suburb priced at PKR 1 crore. You have saved PKR 20 lakh for the down payment. You approach a bank and borrow PKR 80 lakh at a 5% annual markup rate for 20 years (these terms are similar to Pakistan's current Apna Ghar government housing scheme).

Your monthly payment would be approximately PKR 52,800. Over 20 years, you will have paid back the PKR 80 lakh you borrowed plus about PKR 46.7 lakh in total markup. That means the total cost of the house through financing is roughly PKR 1.47 crore (including your down payment).

Is PKR 46.7 lakh a lot to pay in markup? Yes. But consider the alternative: waiting 15 - 20 years to save PKR 1 crore in cash while paying rent the entire time - and potentially watching property prices rise beyond your reach.

How Does a Mortgage Work Step by Step?

I have walked through this process with hundreds of families. Let me break down exactly what happens from the moment you decide to buy a home until the day you make your final payment.

Step 1 – The Down Payment

Before any lender will consider your application, you need to contribute your own money upfront. This is called the down payment, and it is your “skin in the game.”

In Pakistan, typical down payment requirements range from 10% to 25% of the property value. Under the government’s Wazir-e-Azam Apna Ghar Program, you can qualify with as little as 10% down. For example, a PKR 10 million (1 crore) house requires a PKR 1 million down payment from you, with the bank covering the remaining 90%.

In international markets, standard down payments often range from 3% for first-time homebuyer programs to 20% for conventional loans without private mortgage insurance.

Pro Tip: The larger your down payment, the less you borrow, the lower your monthly payments, and the less total markup you pay over the life of the loan. If you can stretch to 20% instead of 10%, I recommend it.

Step 2 – Borrowing from the Lender

Once you know your budget and down payment amount, you formally apply for a mortgage. The lender reviews your income, credit history, existing debts, employment stability, and the value of the property you want to buy. This process is called underwriting.

If approved, the lender issues a commitment letter stating the loan amount, interest rate, term, and monthly payment. You and the seller then proceed to closing.

Step 3 – Interest Charges (Markup)

Interest – called “markup” in Pakistan – is how lenders make money. It is calculated as an annual percentage of your outstanding loan balance. If your loan carries a 5% markup rate, you pay approximately 5% of whatever principal remains unpaid each year, divided across 12 monthly payments.

In the early years of your mortgage, most of each payment goes toward interest, not principal. Why? Because you owe a larger amount early on, and interest is calculated on the full outstanding balance. As years pass and your balance decreases, more of each payment chips away at the principal. This is called amortization.

Step 4 – Monthly Payments

Each month, you make one payment to your lender. That single payment typically bundles together:

- Principal – reduces your loan balance

- Interest/Markup – the lender’s charge

- Property taxes (if held in escrow) – your local government tax obligation

- Insurance (if held in escrow) – protects the property against damage

Together, these four elements form what is called PITI (Principal, Interest, Taxes, Insurance). I will break these down in detail later in this guide.

Step 5 – Loan Payoff and Full Ownership

With each payment, your loan balance decreases. After years of consistent payments – 15, 20, or whatever your term specifies – you reach the final installment. The lender removes the lien from your property title, and you own the house completely.

There is a genuine feeling of accomplishment that comes with that final payment. I have had clients frame their “loan paid in full” letter. It is a milestone worth celebrating.

What Happens If You Miss Mortgage Payments?

This is a question everyone should ask before signing. Missing payments has serious consequences, and the timeline matters.

| Time After Missed Payment | What Happens | Potential Impact |

|---|---|---|

| 1 – 30 Days Late | Late fee may be charged and the lender may contact you for payment. | Minor penalty fees and early warning signs. |

| 30 – 90 Days Late | Account may be marked delinquent, lender increases collection efforts, and missed payments may be reported. | Credit profile can be negatively affected. |

| 90+ Days Late | Loan may enter formal default, and foreclosure or repossession proceedings could begin. | Serious legal and financial consequences. |

| Foreclosure Completed | Lender can take possession of the property and sell it to recover the outstanding debt. | Loss of home and possible long-term credit damage. |

My honest advice: if you ever face a situation where you might miss a payment, contact your lender before it happens. Most banks have hardship programs, temporary payment reductions, or restructuring options. Silence is the worst strategy.

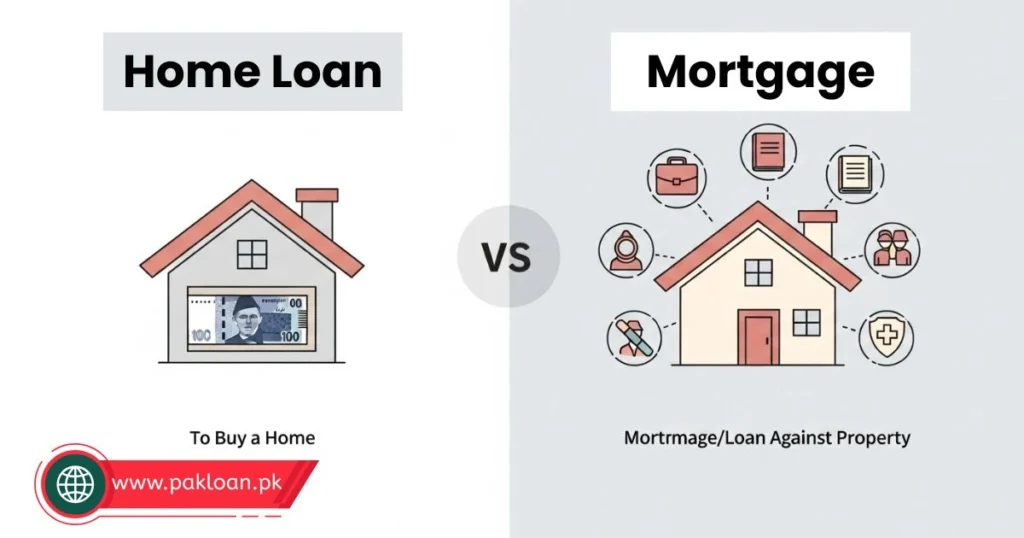

Mortgage vs Home Loan – What’s the Difference?

This confusion is understandable. In casual conversation, people use these terms interchangeably. I have done it myself. But technically, there is a difference worth knowing.

In many South Asian financial contexts, including Pakistan and India, “home loan” and “mortgage loan” are distinct products:

Mortgage vs Home Loan Comparison

| Feature | Home Loan | Mortgage Loan (Loan Against Property) |

|---|---|---|

| Purpose | Used specifically for buying, building, or renovating a residential property. | Can be used for multiple purposes like business, education, medical expenses, or debt consolidation. |

| Property Used as Collateral | The property you are purchasing becomes collateral. | A property you already own is pledged as collateral. |

| Loan-to-Value (LTV) | Can finance up to 90% of property value. | Usually finances 60–75% of property value. |

| Interest Rate | Generally lower, as lenders consider it lower-risk borrowing. | Typically 1–3% higher than home loan rates. |

| Repayment Tenure | Longer repayment periods, often up to 30 years. | Usually shorter, often up to 15 years. |

| Tax Benefits | Often eligible for tax benefits (depends on country laws). | Usually limited or no tax benefits, unless tied to specific business use. |

This table draws from lending practices in Pakistan and India, where the distinction is common.

Are They the Same in Pakistan?

In practice, when Pakistanis talk about getting a “mortgage” or a “home loan” to buy a house, they are referring to the same thing: borrowing money to purchase residential property. Banks like Meezan, UBL Ameen, HBL, and HBFC offer home financing products – loans specifically designed for buying or building a home.

The term “mortgage” in Pakistan often carries a broader legal meaning: it refers to the legal mechanism of pledging property as security for any loan. A “home loan” or “housing finance” is the specific product for buying a home.

Bottom line: if you are looking to buy a house in Pakistan, ask your bank about “housing finance” or “home financing.” That is the product you need. The term “mortgage” is the legal arrangement behind it.

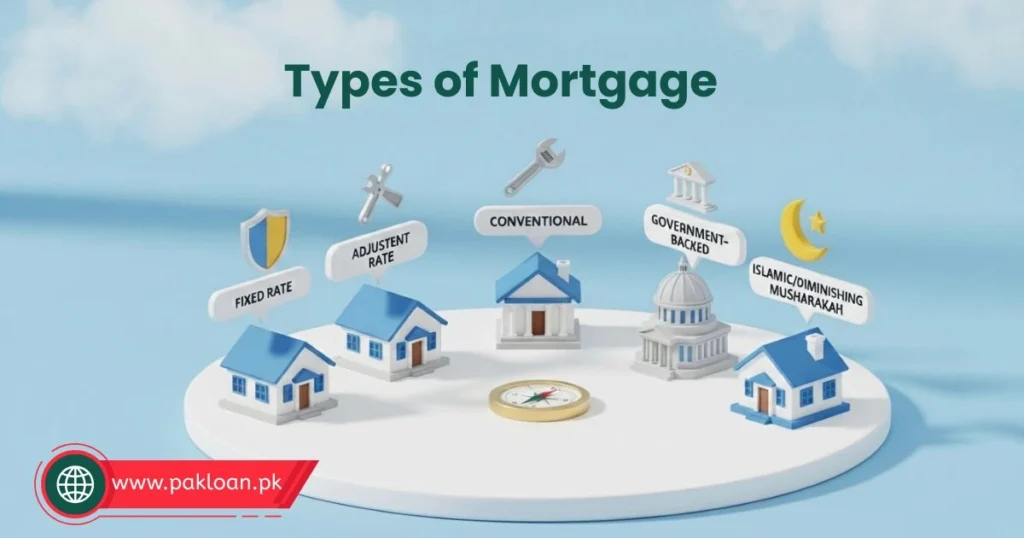

Main Types of Mortgages Beginners Should Know

I have seen borrowers get overwhelmed by the variety of mortgage products available. Let me simplify. Almost every mortgage falls into a few core categories. Understanding these five types will cover 95% of what you encounter.

1. Fixed-Rate Mortgage

With a fixed-rate mortgage, your interest rate never changes – period. Whether market rates go up to 15% or down to 3%, your rate stays the same for the entire loan term.

Available terms: Common fixed-rate terms include 30-year and 15-year options. A 30-year fixed mortgage spreads payments across three decades, keeping monthly installments lower but increasing total interest paid. A 15-year fixed mortgage has higher monthly payments but saves significantly on total interest.

How Fixed Rates Work

In Pakistan, the government-backed Apna Ghar Program offers a fixed end-user rate of 5% for the first 10 years, providing predictability during the most financially vulnerable period of homeownership.

Who Fixed-Rate Mortgages Are Best For

Best for: Borrowers who plan to stay in their home long-term and want payment stability.

2. Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a lower fixed rate for an introductory period – typically 3, 5, or 7 years – and then adjusts periodically based on market conditions.

How ARMs Work

A common structure is the 5/1 ARM: fixed rate for the first five years, then adjustment once per year thereafter. The initial rate is usually lower than a comparable fixed-rate mortgage, which can mean significant savings in the early years. However, once the adjustment period begins, your rate could increase substantially.

Risks and Benefits of Adjustable Rates

In Pakistan, variable-rate mortgages are often linked to KIBOR (Karachi Interbank Offered Rate) plus a bank spread. When KIBOR moves, your installment amount moves with it.

Best for: Borrowers who plan to sell or refinance before the adjustment period begins.

Pro Tip: I generally recommend fixed-rate mortgages for first-time buyers in Pakistan, especially if you are stretching your budget. The peace of mind knowing your payment will not change is worth the potentially slightly higher starting rate. I have seen too many families struggle when variable rates spike.

3. Conventional Mortgage

A conventional mortgage is any home loan not insured or guaranteed by the government. These loans are offered by private lenders like banks and mortgage companies and typically require stronger credit profiles.

Conventional loans often require credit scores of at least 620 and may need private mortgage insurance (PMI) if your down payment is below 20%.

Best for: Borrowers with good credit, stable income, and the ability to make at least a 5 – 20% down payment.

4. Government-Backed Mortgages

These are loans insured or guaranteed by government agencies, making them more accessible to borrowers who might not qualify for conventional financing. Common examples include FHA loans (U.S. Federal Housing Administration) and VA loans (for veterans).

Pakistan’s Apna Ghar Program Explained

In Pakistan, the closest equivalent is the government-subsidized housing finance offered through the Apna Ghar Program / Mera Ghar Mera Ashiana scheme. The State Bank of Pakistan (SBP) provides a partial risk-sharing facility that covers 10% of the outstanding portfolio on a first-loss basis, encouraging banks to lend more freely to first-time homeowners.

Key features of Pakistan’s government-backed program:

- Maximum loan: PKR 10 million

- Fixed markup: 5% for first 10 years

- 90:10 loan-to-value ratio (only 10% down payment required)

- Tenure: Up to 20 years

- Housing unit size: Up to 10 marla (2,720 sq. ft.) for houses; up to 1,500 sq. ft. for apartments

Best for: First-time homeowners with limited savings but stable income.

5. Islamic / Shariah-Compliant Home Financing in Pakistan

This is the most important option I cover with Pakistani clients, and it is an area where many competitors’ mortgage guides fall short.

What Is Diminishing Musharakah?

Islamic home financing avoids interest (riba), which is prohibited under Shariah law. Instead, it uses partnership and lease-based structures. The dominant model in Pakistan is Diminishing Musharakah.

How Islamic Mortgage Financing Works

Joint Ownership: You and the bank become joint owners of the property. If you need 80% financing, the bank owns an 80% share; you own 20%.

Lease Back: The bank leases its share of the property to you. You pay monthly rent for using the bank’s portion.

Gradual Purchase: With each monthly payment, you also buy a small portion of the bank’s share. Over time, your ownership increases and the bank’s decreases — hence “diminishing” Musharakah.

Full Ownership: By the final payment, you have purchased the bank’s entire share, and you become the sole owner.

Major Islamic banks in Pakistan offering this include:

Meezan Bank – Easy Home / Apna Ghar Program

UBL Ameen – Ameen Address Islamic Housing Finance

BankIslami – MUSKUN Home Financing

Askari Bank – Diminishing Musharakah Housing Finance

Best for: Pakistani families seeking Shariah-compliant financing that aligns with Islamic principles.

Quick Comparison: Mortgage Types at a Glance

| Mortgage Type | Best For | Main Advantage | Key Risk |

|---|---|---|---|

| Fixed-Rate | Long-term buyers | Stable payments | May cost more if rates fall |

| Adjustable-Rate (ARM) | Short-term owners | Lower starting rate | Payments may rise later |

| Conventional | Strong credit borrowers | Competitive rates | Tougher approval rules |

| Government-Backed | First-time buyers | Low down payment | Loan/property limits |

| Islamic (Diminishing Musharakah) | Shariah-focused buyers | Interest-free structure | Different fee models |

Understanding Mortgage Rates (Without the Confusion)

Mortgage rates are where I see the most misunderstanding – and the most money left on the table. Let me make this crystal clear.

What Are Mortgage Rates?

A mortgage rate is the annual percentage a lender charges you for borrowing money. It determines how much you pay beyond the principal you borrowed.

Why Small Rate Differences Matter

Even small differences in rates matter enormously over time. Consider this:

| Rate | Monthly Payment | Total Interest Paid |

|---|---|---|

| 5% | ~PKR 42,940 | ~PKR 7.45 million |

| 7% | ~PKR 53,220 | ~PKR 11.16 million |

| 9% | ~PKR 64,350 | ~PKR 15.17 million |

Source: Author calculations using standard amortization. The difference between 5% and 9% on an PKR 8 million loan is approximately PKR 7.7 million in additional interest over 30 years.

The gap between 5% and 9% means paying nearly PKR 7.7 million extra over the life of the loan. That is almost the price of another small house.

What Affects Mortgage Rates?

Several factors determine the rate a lender offers you:

Central bank policy

The State Bank of Pakistan’s monetary policy sets the broad direction. SBP’s policy rate influences KIBOR, which in turn affects mortgage pricing.

Inflation

Higher inflation generally leads to higher rates. Pakistan’s inflation environment directly impacts housing finance costs.

Your credit profile

Better credit scores earn lower rates. Lenders price risk — the riskier you appear, the higher your rate.

Loan term

Shorter-term loans (15 years) usually carry lower rates than longer terms (30 years). In the U.S., a 15-year fixed mortgage in April 2026 averaged 5.75%, compared to 6.38% for a 30-year fixed.

Down payment size

Larger down payments reduce lender risk and can improve your rate.

Loan type

Government-backed loans may offer subsidized rates. Pakistan’s Apna Ghar Program fixes the end-user rate at 5% – significantly below market rates – with the government reimbursing the difference to banks.

Fixed vs. Variable Mortgage Rates

| Feature | Fixed Rate | Variable Rate |

|---|---|---|

| How it works | Interest stays same for full loan term | Changes with market index (e.g., KIBOR) |

| Monthly payment | Stable and predictable | Can increase or decrease |

| Risk | You may miss savings if rates drop | Payments may rise if rates increase |

| Best when | You want stability or rates are low | You can handle changes or expect rates to fall |

Pro Tip: In Pakistan's current environment (2026), the government-subsidized 5% fixed rate under the Apna Ghar Program is exceptionally competitive. Market rates from commercial banks without subsidies are typically KIBOR+3% or higher.

If you qualify for the government scheme, I strongly recommend locking in that 5% rate for the first decade.

A Note on 30-Year Mortgage Rates (2026 Context)

For readers comparing international options, 30-year fixed mortgage rates in the U.S. averaged approximately 6.18% during the first months of 2026, down from above 7% during the same period in 2025. As of late April 2026, the average 30-year fixed rate stood at roughly 6.38%, with some forecasts suggesting rates around 6 – 6.3% through year-end.

These rates serve as a useful benchmark if you are comparing international mortgage options alongside Pakistani housing finance.

What Costs Are Included in a Mortgage?

Your monthly mortgage payment is not just one number. It is built from four primary components, remembered by the acronym PITI: Principal, Interest, Taxes, and Insurance.

PITI Breakdown Chart

| Component | What It Is | How It Works |

|---|---|---|

| Principal | The original loan amount you borrowed | Each payment reduces your remaining loan balance |

| Interest | Cost of borrowing money | Calculated on remaining balance; higher portion early in loan |

| Taxes | Annual property tax (if applicable) | Collected monthly and held in escrow, paid yearly |

| Insurance | Home/property insurance | Protects against damage, fire, or natural disasters |

Each Component Explained

Principal: If you borrow PKR 8 million, that amount is your principal. Each month, a portion of your payment goes toward reducing this balance. In the early years, only a small fraction of each payment hits the principal; the rest covers interest.

Interest: This is the lender’s profit. On a PKR 8 million loan at 5%, your annual interest in year one is roughly PKR 400,000 – about PKR 33,000 per month. As your balance decreases, so does the interest portion of each payment.

Property Taxes: In Pakistan, property tax (also called “house tax” or “municipal tax”) varies by province and city. Punjab, Sindh, KPK, and Balochistan each have their own property tax systems. Rates are generally quite low compared to international standards – often less than 1% of property value annually for residential properties. In many Pakistani mortgage arrangements, property taxes are paid directly by the homeowner rather than through escrow.

Homeowners Insurance: This protects your property against fire, floods, earthquakes, and other damage. In Pakistan, home insurance is available through most major insurers and is typically required by lenders (including Islamic banks) as a condition of financing.

Closing Costs You Should Know

Beyond your monthly payment, there are one-time costs when you finalize the mortgage. These are called closing costs and typically range from 3% to 6% of the loan amount.

In Pakistan, common closing costs include:

| Cost Item | Approximate Range |

|---|---|

| Legal / Documentation Charges | At actual cost (varies by bank/lawyer) |

| Property Valuation Charges | At actual cost (varies by property size/value) |

| Processing Fees | Varies (often waived in government schemes) |

| Stamp Duty & Registration | Varies by province and property value |

| Title Search & Verification | Varies based on legal checks required |

Important: Under the Apna Ghar Program, processing fees are waived (NIL), and there are no prepayment penalties. This makes the government scheme particularly attractive for first-time buyers.

How Beginners Qualify for a Mortgage

What lenders really want to know before approving your application can be summarized in a few key factors. I have reviewed thousands of applications and seen what works.

The Key Factors Lenders Evaluate

1. Credit Score and Credit History

Your credit score is a three-digit number that summarizes how reliably you have handled borrowed money in the past. In Pakistan, credit information is maintained by the e-CIB (Electronic Credit Information Bureau) under the State Bank of Pakistan. Banks check your e-CIB report during the application process.

For conventional loans internationally, a minimum credit score of 620 is typical, though government-backed FHA loans may accept scores as low as 580, or even 500 with a higher down payment.

In Pakistan, lenders look for:

No history of loan defaults, write-offs, or waivers

Clean repayment history on existing credit cards and loans

Negative history remains on e-CIB for two years after settlement

Pro Tip: Before applying for housing finance in Pakistan, request your own e-CIB report from your bank. Check it for errors and address any issues before the lender sees them.

2. Income Requirements

Lenders need confidence that you can afford the monthly payments. They look at:

Your gross monthly income

Employment stability (minimum 6 months continuous work for salaried individuals in Pakistan; 2 years for self-employed)

For the Apna Ghar Program, minimum gross income of PKR 40,000 per month is required

3. Debt-to-Income (DTI) Ratio

This measures how much of your monthly income goes toward debt payments. If you earn PKR 100,000 per month and your total debt payments (including the proposed mortgage) are PKR 45,000, your DTI is 45%.

Under Pakistan’s revised prudential regulations for the Apna Ghar Program, the State Bank of Pakistan has relaxed the debt burden ratio to allow total monthly repayment obligations – including the new housing loan and existing consumer debt – to reach up to 65% of a borrower’s net disposable income. This significantly expands eligibility compared to earlier, more restrictive limits.

4. Down Payment Requirements

You need cash available for the down payment. Under Pakistan’s government scheme, only 10% of the property value is required from you (90:10 loan-to-value ratio). On a PKR 10 million home, that means PKR 1 million from your own funds.

For conventional loans, typical requirements range from 3% to 20%, with 20% being the threshold at which private mortgage insurance (PMI) is no longer required.

Beginner Mortgage Qualification Checklist

Use this checklist to assess your readiness before approaching a lender:

CNIC: Valid CNIC (Computerized National Identity Card) – mandatory in Pakistan

Credit History: No defaults, write-offs, or waivers on e-CIB report in the past two years

Income: Stable income – minimum 6 months work history (salaried) or 2 years (self-employed)

Gross Monthly Income: At least PKR 40,000 (for Apna Ghar Program); higher for larger loans

DTI Ratio: Total monthly debt payments (including proposed mortgage) within 65% of net disposable income (for Apna Ghar Program)

Down Payment: 10% of property value saved (for government scheme); 20%+ for conventional

Property Documents: Clean title, no disputes, proper registration

Age: Between 20 and 65 years at loan maturity (varies by lender)

First-Time Homeowner: Yes (for government-subsidized schemes)

Employment: In a recognized field or business with verifiable income

Documents You Usually Need

When you apply for housing finance in Pakistan, have these documents ready:

| Document | Salaried Applicant | Self-Employed / Business |

|---|---|---|

| CNIC Copy | Required | Required |

| Passport Photos | Required | Required |

| Salary Slips | Last 3–6 months | — |

| Bank Statements | Last 6 months | Last 6–12 months |

| Employment Letter | Required | — |

| Business Proof | — | Registration / NTN |

| Tax Returns | If applicable | Last 1 – 2 years |

| Property Documents | Title, registry, tax receipts | Same |

| e-CIB / Credit Report | Pulled by bank | Same |

Common Mortgage Mistakes Beginners Should Avoid

I have watched smart, educated people make completely avoidable mistakes. Here are the ones that surface again and again – and how you can sidestep them.

1. Borrowing More Than You Can Afford

Banks may approve you for more than you should actually borrow. Just because the lender says you are eligible for PKR 10 million does not mean you should borrow the full amount. Remember: lenders calculate what you can pay, not what you will comfortably pay while also handling life’s other expenses – school fees, medical costs, utilities, and savings.

My rule of thumb: your total housing payment (mortgage installment plus taxes and insurance) should not exceed 30 – 35% of your take-home income. Government schemes may allow up to 65%, but that is a ceiling, not a recommendation.

2. Ignoring Hidden and Ongoing Costs

The down payment and monthly installment are just the start. First-time buyers often overlook:

- Stamp duty and registration fees – property transfer taxes that vary by province

- Legal and documentation charges – lawyer fees for title verification

- Property valuation fees – lender-required assessment of the property’s worth

- Homeowners insurance – annual premiums

- Maintenance and repairs – houses need upkeep, and that costs money

- Utility connections and deposits – gas, electricity, water

Set aside an additional 5–7% of the property value beyond your down payment for these costs.

Pro Tip: When I help clients budget, I ask them to list every possible cost on paper before committing. The exercise usually reveals PKR 300,000 - PKR 500,000 in expenses they had not considered on a PKR 10 million purchase.

3. Not Comparing Lenders and Rates

Getting just one quote and accepting it is one of the most expensive shortcuts you can take. I have seen rate differences of 1 – 2 percentage points between lenders in Pakistan for similar loan profiles. Over 20 years, that difference compounds into lakhs of rupees in additional costs.

In international markets, comparing quotes from at least three lenders is a standard practice recommended by consumer finance experts. Even a small rate difference can save you a substantial amount over time. For example, on a $350,000 mortgage, reducing your interest rate by just 0.5% could save you around $35,000 in interest over a 30-year loan term. That’s why shopping around before choosing a lender can be one of the smartest financial decisions you make.

4. Choosing the Wrong Loan Term

A longer term (25–30 years) means lower monthly payments but far more total interest. A shorter term (15 years) means higher monthly payments but dramatic interest savings. The right choice depends on your budget, income trajectory, and long-term plans.

5. Misunderstanding Interest Rates and Markup Structures

This mistake is particularly common in Pakistan, where Islamic and conventional products use different terminology. A “rental rate” of 5% under Diminishing Musharakah is not the same as a “markup rate” of 5% under conventional financing – the calculation methods differ. Make sure the lender explains, in writing, exactly how your payments are calculated.

Pros and Cons of Getting a Mortgage

A mortgage is neither inherently good nor bad. It is a financial tool, and like any tool, its value depends on how you use it and whether it fits your situation. Here is an honest assessment based on what I have observed over the years.

| Pros of a Mortgage | Potential Cons |

|---|---|

| Makes Homeownership Possible: Buy a home now instead of waiting years to save full cash. | Large Long-Term Debt: A mortgage is often your biggest financial commitment. |

| Builds Equity Over Time: Each payment increases your ownership in the property. | Interest/Markup Costs: You may repay much more than the original loan amount. |

| Property May Appreciate: Your home’s value could grow over time. | Property Value Risk: Market declines can create negative equity. |

| Stable Payments (Fixed Rate): Predictable housing costs for years. | Foreclosure Risk: Missed payments could put your home at risk. |

| Can Strengthen Credit: On-time payments may improve your credit profile. | Less Flexibility: Selling a financed property can be more complicated. |

| Possible Tax Benefits: Mortgage-related deductions may apply in some countries. | Upfront Costs: Closing costs, duties, and fees add to purchase costs. |

My honest take: for most middle-class families in Pakistan, a mortgage (or Islamic home financing) is the only practical path to homeownership. The key is not avoiding mortgages altogether – it is choosing the right mortgage for your specific financial situation and staying well within your means.

Mortgage Example (Real Beginner Scenario)

Let me walk you through a realistic example that puts all these numbers into perspective. I will use a scenario comparable to both Pakistani and international contexts.

Ahmed’s Home Buying Scenario

Ahmed is a 32-year-old software professional in Islamabad. He earns PKR 150,000 per month and has saved PKR 2 million (20 lakh) over the past five years. He wants to buy a 10-marla house in a developing area priced at PKR 10 million (approximately $100,000 equivalent).

Ahmed’s Financial Snapshot:

Monthly income: PKR 150,000

Savings (down payment): PKR 2,000,000 (20%)

Existing monthly debt payments: PKR 15,000 (car loan)

Proposed loan amount: PKR 8,000,000

Rate: 5% fixed (using Apna Ghar Program subsidized rate) for first 10 years

Term: 20 years

Monthly Payment Breakdown

| Payment Component | Estimated Monthly Amount |

|---|---|

| Principal & Markup | ~PKR 52,800 |

| Property Taxes | ~PKR 2,500 |

| Home Insurance | ~PKR 1,500 |

| Total Monthly Payment | ~PKR 56,800 |

Does This Fit Ahmed’s Budget?

| Budget Metric | Amount / Ratio |

|---|---|

| Monthly Income | PKR 150,000 |

| Existing Car Loan | PKR 15,000 |

| Mortgage Payment | PKR 56,800 |

| Total Monthly Debt Payments | PKR 71,800 |

| Debt-to-Income Ratio (DTI) | 47.9% |

| Remaining for Living Expenses | PKR 78,200 |

With Pakistan’s relaxed DTI limit of 65%, Ahmed qualifies comfortably. His housing payment accounts for about 38% of his gross income – within the healthier 30 – 35% target range.

The Long-Term Cost of the Mortgage

| Amount | Value |

|---|---|

| Original Loan (Principal) | PKR 8,000,000 |

| Total Payments (20 Years) | ~PKR 12,672,000 |

| Total Markup / Interest Paid | ~PKR 4,672,000 |

| Down Payment | PKR 2,000,000 |

| Total Home Cost (Including Down Payment) | ~PKR 14,672,000 |

Ahmed will pay approximately PKR 4,672,000 in markup over 20 years. That is real money – but consider the alternative: renting a comparable house for PKR 35,000–40,000 per month (increasing yearly) for 20 years would cost PKR 8.4 – 9.6 million with zero ownership or equity at the end.

Pro Tip: This example uses the subsidized 5% rate. At current commercial bank rates (KIBOR + 3%, roughly 10–12%), the same loan would have a monthly payment closer to PKR 76,000 - 88,000. This is why I urge all eligible first-time buyers in Pakistan to explore the government-backed Apna Ghar Program before considering commercial options.

Mortgage in Pakistan – What Beginners Should Know

Pakistan’s mortgage market is unique, and understanding its landscape will save you from costly surprises.

How Mortgages Work in Pakistan

Home financing in Pakistan operates through several channels:

Commercial banks: HBL, UBL, Bank Alfalah, Standard Chartered, and others offer conventional mortgage products

Islamic banks: Meezan Bank, BankIslami, Dubai Islamic Bank, UBL Ameen, and others offer Shariah-compliant Diminishing Musharakah products

House Building Finance Company (HBFC): a government-owned institution established in 1952, focused on affordable housing for low and middle-income groups

Microfinance banks: participating in government schemes to reach lower-income segments

The State Bank of Pakistan regulates all housing finance through its prudential regulations for housing finance (HF series). In 2026, SBP has actively relaxed requirements to stimulate the market, including:

- Raising the maximum loan limit from PKR 3.5 million to PKR 10 million

- Reducing the subsidized markup rate from as high as 8% to a flat 5%

- Relaxing debt burden ratio limits to 65% of net disposable income

- Mandating credit approval within 15 working days for complete applications

- Waiving processing fees and prepayment penalties under government schemes

Banks Offering Mortgage Financing

| Institution | Type | Key Product | Rate / Structure |

|---|---|---|---|

| Meezan Bank | Islamic | Easy Home / Apna Ghar | 5% fixed (10 yrs), Diminishing Musharakah |

| UBL Ameen | Islamic | Ameen Address | Diminishing Musharakah, KIBOR-linked |

| HBL | Conventional + Islamic | HBL Home Finance | Varies by product |

| BankIslami | Islamic | MUSKUN Home Financing | Diminishing Musharakah |

| Askari Bank | Islamic | Housing Finance | Competitive rental rates |

| HBFC | Government-backed | Ghar for HER & others | Affordable tiered rates |

| Standard Chartered | Conventional | Mortgage / Home Loan | Market-linked rates |

Islamic Alternatives in Detail

For many Pakistani families, Shariah compliance is non-negotiable. The Diminishing Musharakah model is the industry standard for Islamic home financing in Pakistan.

How Diminishing Musharakah works, step by step:

- You identify a property you want to buy

- You and the bank enter into a Musharakah (partnership) agreement

- The bank contributes its share (e.g., 80% of the price); you contribute your share (e.g., 20%)

- You both become joint owners of the property

- The bank leases its share to you for a monthly rental

- Each month, you purchase a small unit of the bank’s share alongside paying rent

- Over time, the bank’s ownership decreases, yours increases

- When the final payment is made, the bank’s share reaches zero, and you own 100%

- The monthly “installment” under this structure has two components:

- Rental payment for using the bank’s share (analogous to interest, but structured as rent)

- Unit purchase – buying the bank’s equity (reducing the bank’s ownership)

Things to Compare Before Applying in Pakistan

| Factor | What to Check |

|---|---|

| Markup / Rental Rate | Fixed or variable? KIBOR-linked or subsidized? |

| Processing Fees | Bank charges vs fee waivers under government schemes |

| Prepayment Terms | Can you pay early without penalties? |

| Insurance Requirements | Takaful (Islamic) or conventional insurance |

| Maximum Financing | What percentage of property value is financed? |

| Tenure Flexibility | Available minimum and maximum repayment terms |

| Property Eligibility | Restrictions on property type, size, or location |

Documentation requirements Exactly what paperwork is needed for approval

How to Choose the Right Mortgage as a Beginner

After years of counseling borrowers, I have distilled the mortgage selection process into a clear decision framework.

Step 1: Define Your Budget Honestly

Before approaching any lender, know your numbers:

- What is your monthly take-home income?

- What are your fixed monthly expenses?

- How much have you saved for a down payment?

- How much can you comfortably allocate to housing each month?

- Do not let a lender’s approval amount dictate your budget. Set your own ceiling.

Step 2: Compare Rates Across Lenders

Rate differences can be substantial. Get quotes from at least three different institutions – ideally a mix of conventional banks and Islamic banks. Compare not just the headline rate but the full annual percentage cost including all fees.

Step 3: Pick the Right Term

| If You Want… | Consider… |

|---|---|

| Lowest Monthly Payment | Longer term (20 – 25 years) |

| Lowest Total Borrowing Cost | Shorter term (10 – 15 years) |

| Balance of Cost & Affordability | Medium term (15 – 20 years) |

Step 4: Get Pre-Approved

Pre-approval is a written commitment from a lender stating how much they are willing to lend you, subject to final verification. It gives you:

- A clear budget for house hunting

- Credibility with sellers and real estate agents

- A faster final approval process

Step 5: Compare Lenders Beyond Rates

Rate is important, but also evaluate:

- Customer service responsiveness

- Processing speed (SBP now mandates 15 working days for Apna Ghar applications)

- Branch accessibility in your city

- Flexibility for prepayment and restructuring

- Reputation and complaint resolution record

Mortgage Decision Checklist

- ☐ I have defined my maximum affordable monthly payment

- ☐ I have saved at least 10–20% of the target property value for a down payment

- ☐ I have budgeted for additional costs (stamp duty, legal, maintenance, insurance)

- ☐ I have obtained quotes from at least three lenders

- ☐ I have compared both conventional and Islamic options

- ☐ I understand the difference between fixed and variable rates

- ☐ I know the total markup/rental cost over the full loan term

- ☐ I have checked my credit history (e-CIB report)

- ☐ I have the required documents ready

- ☐ I have chosen a loan term I can comfortably sustain

- ☐ I have been pre-approved before starting serious house hunting

Beginner Mortgage Checklist Before Applying

Use this downloadable-style checklist to ensure you are prepared before submitting any application.

Financial Readiness

- Down payment saved: At least 10% of your target property value

- Emergency fund: 3 – 6 months of living expenses set aside (separate from the down payment)

- Stable income: At least 6 months in current job/business (salaried) or 2 years (self-employed)

- DTI calculation: Total monthly debts, including the proposed mortgage, within an acceptable range – ideally under 50% but up to 65% allowed under Apna Ghar

Credit Readiness

- e-CIB check: Reviewed your credit report for errors and negative entries

- No recent defaults: Clean repayment history on all existing loans and credit cards

- Credit card balances: Paid down or at manageable levels

Documentation Readiness

- CNIC copies (applicant and co-applicant)

- Passport-size photographs

- Last 6 months’ bank statements

- Salary slips (last 3–6 months) or business income proof

- Employment confirmation letter (salaried) or business registration documents (self-employed)

- Property documents (title deed, tax receipts, etc.)

- Tax returns (if applicable)

Knowledge Readiness

- I understand the type of mortgage/financing I am applying for (conventional or Islamic)

- I understand how my markup/rental rate is calculated

- I know the total cost of the loan over its full term

- I know what happens if I miss payments

- I have a clear picture of all upfront and ongoing costs

Frequently Asked Questions

What is a mortgage in simple words?

A mortgage is a loan you take to buy a house or property. You borrow money from a bank or financial institution, and you pay it back in monthly installments over many years – typically 15 to 25. The property itself serves as security for the loan, meaning the lender can take possession if you fail to make payments.

How does a mortgage work?

A mortgage works like this: you make a down payment (your own contribution toward the property price), and a lender covers the rest. You then repay the loan in fixed monthly payments that include both the principal (the amount you borrowed) and interest/markup (the lender’s charge).

Each payment reduces your loan balance. After the final payment, the lender’s claim on the property is removed, and you own the home outright.

What are the different types of mortgages?

The main types are:

(1) Fixed-rate mortgages – same interest rate for the entire loan term,

(2) Adjustable-rate mortgages (ARMs) – rate starts low and adjusts periodically based on market conditions,

(3) Conventional mortgages – standard loans from private lenders without government backing,

(4) Government-backed mortgages – insured by government agencies (like FHA in the U.S. or Pakistan’s Apna Ghar Program), and

(5) Islamic/Shariah-compliant financing – using partnership models like Diminishing Musharakah instead of interest.

What is the difference between a mortgage and a home loan?

Technically, a “mortgage” is the legal agreement that pledges property as security for a loan, while a “home loan” is money borrowed specifically to buy or build a residential property. In everyday usage, however, the terms are used interchangeably.

In Pakistan, the distinction is clearer: a “home loan” or “housing finance” is the product you need to buy a house; “mortgage” refers to the legal mechanism securing the loan.

How can beginners qualify for a mortgage?

Beginners qualify by meeting several key requirements: a stable, verifiable income (minimum 6 months employment history for salaried workers), a reasonable debt-to-income ratio (total monthly debts under 65% of income under Pakistan’s relaxed rules),

a clean credit history with no recent defaults, a down payment of at least 10% (or as low as 3–5% in some international programs), and valid identification documents. Government-backed programs often have more lenient qualification standards than conventional loans.

Is a mortgage good or bad?

A mortgage is a financial tool – neither inherently good nor bad. The advantages include making homeownership accessible, building equity over time, and providing payment stability. The disadvantages include taking on significant long-term debt, paying substantial interest/markup over the loan’s life, and the risk of foreclosure if you cannot keep up with payments.

Whether a mortgage is right for you depends on your financial stability, income prospects, and the specific terms of the loan you can secure.

What credit score do I need?

For conventional loans internationally, most lenders require a minimum credit score of 620. Government-backed FHA loans may accept scores as low as 580 (or 500 with a 10% down payment). In Pakistan, rather than a numeric credit score, lenders check your e-CIB report for defaults, late payments, write-offs, and waivers. A clean history is essential for approval.

Can I get a mortgage with low income?

Yes. In Pakistan, the Apna Ghar Program requires a minimum gross monthly income of just PKR 40,000 for salaried individuals. Microfinance banks and HBFC also offer products targeted at lower-income segments. The key is having stable, verifiable income – even if the amount is modest – and keeping your total debt obligations within the lender’s acceptable ratio.

Conclusion: Should You Get a Mortgage as a Beginner?

If you have read this far, you now understand more about mortgages than most first-time buyers walking into a bank. Let me leave you with a clear, honest framework for making your decision.

Who a Mortgage May Suit

A mortgage or home financing arrangement is worth serious consideration if:

- You have stable, predictable income and confidence in your employment or business

- You have saved a meaningful down payment (at least 10%, ideally more)

- You plan to stay in the same home for at least 5 – 7 years

- Your total housing payment would be within 30 – 40% of your take-home income

- You have factored in the full cost – not just the installment, but taxes, insurance, maintenance, and closing costs

- You have compared multiple lenders and understand the terms you are signing

Who Should Wait Before Taking a Mortgage

You may want to delay getting a mortgage if:

- Your income is uncertain or irregular

- You have significant existing debt that already strains your budget

- Your credit history has recent negative entries that need time to clear

- You have not saved enough for both a down payment and an emergency fund

- You plan to relocate within the next 2 – 3 years

- You are feeling pressured rather than confident about the decision

Your Next Steps Before Applying

- Pull your e-CIB report and review your credit standing

- Calculate your affordable monthly payment using a mortgage calculator

- Research the Apna Ghar Program if you are a first-time Pakistani home buyer – the 5% subsidized rate is unlikely to be beaten by commercial options

- Approach at least three lenders for preliminary discussions and rate quotes

- Gather your documents and seek pre-approval before starting your property search

Homeownership is one of the most significant financial decisions you will ever make. It deserves your full attention, your honest self-assessment, and your willingness to ask tough questions. But done right – with the right mortgage, at the right price, on terms you truly understand – it can be the foundation of lasting financial security.

Disclaimer:

Educational Purpose Notice

This article is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Mortgage and home financing terms, rates, and eligibility criteria vary by lender, program, and jurisdiction.

Financial and Legal Advice Disclaimer

Always consult directly with qualified financial institutions, review official State Bank of Pakistan circulars for the latest regulatory updates, and consider speaking with a licensed financial advisor before making any borrowing decision.

You may also like: Complete Guide: Apni Chat Apna Ghar Scheme 2026 Apply Online

Inactivity reset active (10m)