Introduction

For millions of Pakistanis, owning a car is more than just a convenience; it’s a milestone, a symbol of progress, and a key to unlocking new opportunities for family and work. However, with the rising costs of new and used vehicles, paying the full amount upfront has become a distant dream for many. This is where car financing steps in as a powerful tool, turning that dream into an achievable reality. Pakistani banks have developed a range of car financing products designed to fit different budgets and needs, making the journey to car ownership smoother than ever.

But with so many options available, a critical question arises: which is the best bank for car financing in Pakistan? The answer isn’t one-size-fits-all. The right choice depends on your financial situation, your preferences for Islamic or conventional banking, and the specific features you value, such as low markup rates, quick approval, or flexible tenures. Choosing the wrong bank can lead to unnecessary financial strain, hidden charges, and a stressful experience.

You may also like: Meezan Bank Car Installment Calculator - Know your Installment

This in-depth guide for 2025 is designed to be your ultimate resource. We will dissect the car financing landscape in Pakistan, compare the top banks head-to-head, analyze their markup rates and terms, and shine a light on both conventional and Shariah-compliant alternatives. By the end of this article, you will be equipped with all the knowledge needed to confidently select the best bank for car financing in Pakistan for your unique circumstances.

Understanding Car Financing in Pakistan

2.1 What Is Car Financing?

In simple terms, car financing is a loan you take from a bank or financial institution to purchase a vehicle. Instead of paying the entire price of the car at once, the bank pays the dealer on your behalf. You then repay the bank in manageable monthly installments over a predetermined period, known as the tenure. This arrangement includes the principal amount (the actual cost of the car) and a profit for the bank, which is called markup in Islamic banking or interest in conventional systems. Key components include:

Down Payment: This is your initial, upfront contribution. In Pakistan, it typically ranges from 15% to 30% of the car’s ex-factory price. A higher down payment means you borrow less, leading to lower monthly installments.

Tenure: This is the loan repayment period, usually extending from 3 to 7 years. A longer tenure reduces your monthly payment but increases the total markup you pay over the life of the loan.

2.2 Why People Choose Bank Car Financing

Bank financing has become the go-to method for car acquisition in Pakistan due to its numerous benefits:

Convenience: It breaks down a massive financial burden into smaller, budget-friendly monthly payments.

Vehicle Ownership Flexibility: You get to drive and use the car as your own from day one, unlike leasing.

Access to Better Vehicles: It allows you to afford a newer, safer, and more reliable model than what you might be able to buy with cash.

2.3 Importance of Selecting the Best Bank for Car Financing in Pakistan

All banks are not created equal when it comes to auto finance. The differences can have a significant impact on your finances and overall experience.

Markup Rates: Even a slight difference in the markup rate can translate into savings (or costs) of tens of thousands of rupees over the loan’s term.

Approval Time: Some banks are known for their swift, digitized processes, while others may take weeks, potentially causing you to miss out on a good deal.

Customer Support: Responsive and helpful customer service is crucial for resolving queries and issues throughout your loan tenure.

Selecting the wrong bank can lock you into a high-cost agreement with poor service, making what should be an exciting purchase a source of constant frustration.

Useful Tip: Before you start looking at cars, use online car loan calculators (available on every bank's website) to get a realistic idea of what your monthly budget can handle. This will set a clear price range for your vehicle search.

You may also like: Meezan Bank Car Financing 2026 - New Policy New Perks!

Factors to Consider Before Choosing the Best Bank for Car Financing in Pakistan

Making an informed decision requires careful evaluation of several key factors.

3.1 Markup Rates and Total Cost

The markup rate is the most critical factor. Always look at the effective markup rate and calculate the total cost of the loan (principal + total markup). Banks may offer fixed rates, which remain constant throughout the tenure, or variable rates, which can fluctuate with market conditions. In a high-inflation environment like Pakistan’s, a fixed rate provides valuable certainty.

3.2 Down Payment Requirements

Banks typically require a down payment of 15% to 30%. If you can afford a larger down payment, do it. For example, on a PKR 3,000,000 car, a 30% down payment (PKR 900,000) versus a 15% one (PKR 450,000) significantly reduces the amount you need to finance, thereby lowering your monthly financial burden.

3.3 Loan Tenure Options

Tenures generally range from 3 to 7 years. While a 7-year loan offers the lowest monthly installment, you will end up paying much more in total markup. A 5-year tenure is often considered a good balance between affordability and total cost.

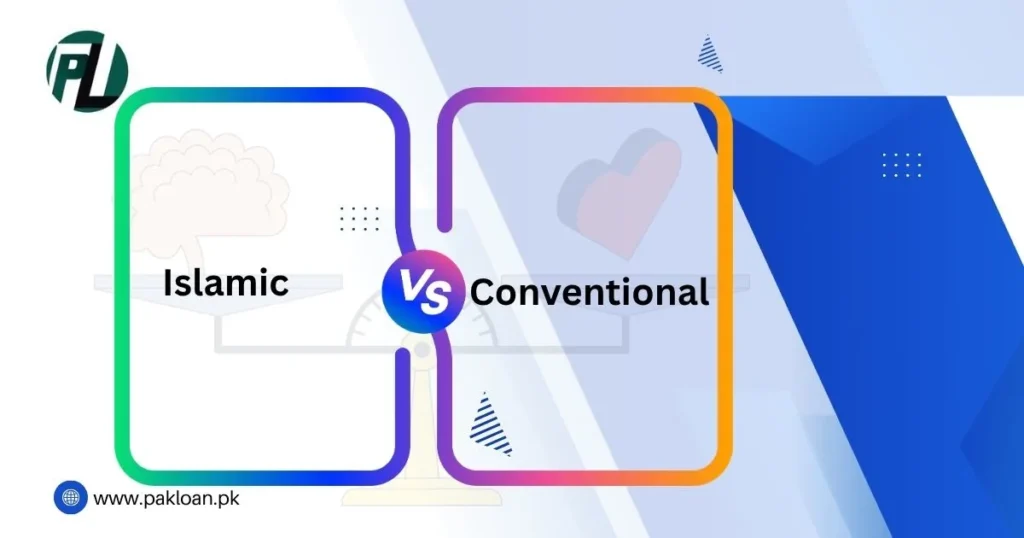

3.4 Islamic vs. Conventional Car Financing

This is a major differentiator in Pakistan.

Conventional Financing is based on interest (Riba).

Islamic Financing uses Shariah-compliant models like Murabaha (cost-plus profit sale) or Ijarah (leasing agreement). In Ijarah, the bank buys the car and leases it to you for a fixed monthly rental, with ownership transferring to you at the end of the term. Many Pakistanis prefer this for its religious permissibility and transparent structure.

3.5 Eligibility Criteria

Each bank has its own set of rules. Common requirements include:

- Minimum Monthly Income: Usually between PKR 30,000 to PKR 50,000.

- Job Type: Specific policies for salaried individuals and self-employed professionals.

- Age Limit: Typically, the applicant must be between 21 and 65 years old at the time of loan maturity.

3.6 Documentation and Approval Process

The standard documents required are CNIC copy, salary slips or proof of business income, and bank statements. Many banks now offer online application portals, drastically reducing processing time from several weeks to just a few days.

Useful Tip: If you are self-employed, keep your bank statements for the last 6 months and business proof documents (e.g., chamber of commerce certificate, sales tax registration) ready. This will speed up the verification process.

You may also like: Shocking truth about the most popular loan apps in Pakistan

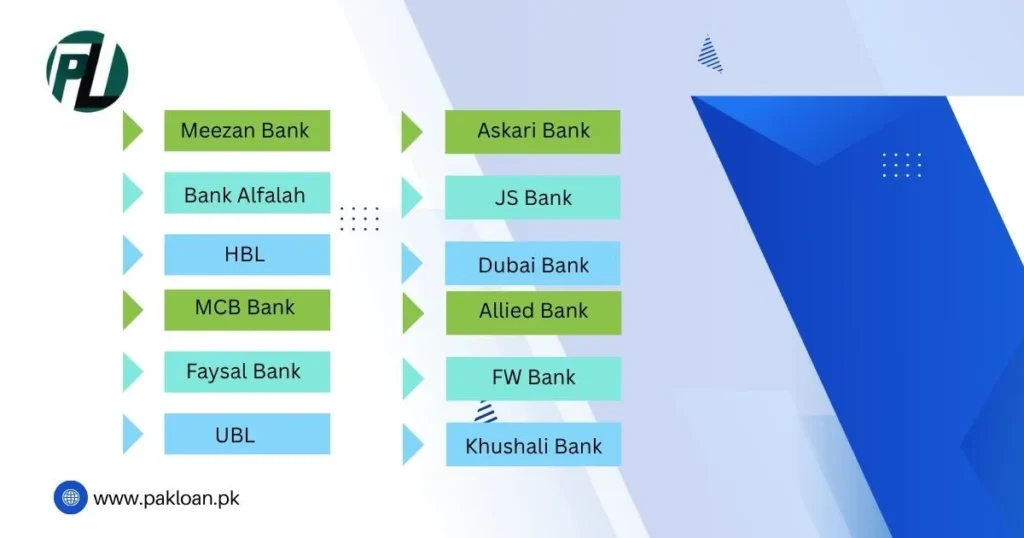

List of the Best Banks for Car Financing in Pakistan Right Now

Here is a detailed breakdown of the top contenders for the title of the best bank for car financing in Pakistan.

4.1 Meezan Bank – The Best Islamic Bank for Car Financing in Pakistan

Meezan Bank is the pioneer and market leader in Islamic banking in Pakistan. Its Car Ijarah product is immensely popular among consumers who seek a Riba-free financing solution.

Overview: The bank purchases the car and leases it to you for a fixed period. You pay a monthly rental, and at the end of the term, the ownership is transferred to you for a pre-agreed price (often a token amount).

Features: Fully Shariah-compliant, transparent rental structure, and easy early settlement options. They have partnerships with all major car manufacturers.

Markup Rate & Tenure: They often offer highly competitive rates, recently around 13% per annum, with tenures of up to 7 years.

Best For: Muslim consumers who strictly prefer Shariah-compliant banking solutions.

✅ Pros and ❌ Cons

✅ Fully Shariah-compliant and trusted.

✅ Competitive profit rates.

✅ Wide network and brand recognition.

❌ Documentation process can be slightly more rigorous.

❌ May not always have the fastest approval time.

4.2 Bank Alfalah – Best Bank for Car Financing in Pakistan for Fast Approval

Bank Alfalah has built a strong reputation for its efficient and customer-friendly auto finance services, often leading the pack in processing speed.

Overview: Alfalah Car Finance offers solutions for both new and used cars with a streamlined online application process.

Features: Known for quick processing (as little as 3-5 days), a user-friendly online portal, and flexible tenures extending to 7 years.

Markup Rate & Tenure: Their rates are competitive, hovering around 14%, and they finance up to 85% of the car’s value.

Best For: Individuals who value speed and a digital, hassle-free application process.

✅ Pros and ❌ Cons

✅ One of the fastest approval times in the market.

✅ Excellent digital experience.

✅ Financing available for used cars.

❌ Markup rates can be slightly higher than some Islamic banks.

❌ Eligibility criteria may be stricter for self-employed applicants.

4.3 HBL (Habib Bank Limited) – Best Bank for Car Financing in Pakistan for Brand Variety

As one of Pakistan’s largest banks, HBL has extensive partnerships with automotive players, giving its customers a wide array of choices.

Overview: HBL CarLoan is a robust product with tie-ups with major brands like Toyota, Suzuki, Honda, Hyundai, and others.

Features: They often run exclusive promotional campaigns with dealers, offering low or zero markup for the initial period. Their disbursement process is also quick once approved.

Markup Rate & Tenure: Rates are around 15%, with a maximum tenure of 5 years for used cars and 7 for new ones.

Best For: Customers who want flexibility in choosing their car brand and want to leverage bank-dealer promotions.

✅ Pros and ❌ Cons

✅ Extensive brand partnerships and variety.

✅ Strong nationwide presence.

✅ Regular promotional offers.

❌ Markup rates can be on the higher side compared to competitors.

❌ The process can be slower than dedicated digital players.

4.4 MCB Bank – Best Bank for Car Financing in Pakistan for Salaried Individuals

MCB Bank offers tailored products, particularly favoring salaried individuals, especially those who already bank with them.

Overview: MCB Car4U provides financing for a range of new and used vehicles.

Features: They offer preferential markup rates for customers who maintain their salary accounts with MCB. Their online tools, like the installment calculator, are very helpful for planning.

Markup Rate & Tenure: Rates are around 14.5%, but can be lower for existing customers. Tenure goes up to 7 years.

Best For: Salaried professionals, especially existing MCB account holders.

✅ Pros and ❌ Cons

✅ Attractive rates for salary account holders.

✅ User-friendly digital platforms.

✅ Good customer service.

❌ Limited benefits for non-account holders.

❌ Less focused on self-employed individuals.

4.5 UBL Bank – Best Bank for Car Financing in Pakistan for Used Cars

UBL Drive has carved a niche for itself with strong offerings for both new and used car financing, making it a top choice for pre-owned vehicle buyers.

Overview: UBL Drive provides financing for a wide age range of used cars, which many other banks are hesitant to finance.

Features: They have a transparent evaluation process for used cars and offer competitive insurance packages bundled with the finance.

Markup Rate & Tenure: Their rates are competitive with the market. They are known for their flexibility in financing older models.

Best For: Individuals looking to purchase a used car with flexible age limits.

✅ Pros and ❌ Cons

✅ Excellent and flexible options for used cars.

✅ Competitive insurance deals.

✅ Straightforward application process.

❌ New car financing offers may be less aggressive than competitors.

❌ Branch service quality can vary.

Useful Tip: When applying for used car financing, always get a trusted mechanic to inspect the vehicle. The bank's evaluation is for its financial security, not the car's mechanical condition.

You may also like: How to get Meezan Bank Car Loan approved in SEVEN(7) days!

4.6 Askari Bank – Best Bank for Car Financing in Pakistan for Military & Govt Employees

Askari Bank has a historic legacy of serving the armed forces, and this reflects in its specialized products for specific segments.

Overview: Askari Car Finance offers customized plans with relaxed terms for military personnel and government employees.

Features: They provide exclusive packages, sometimes with lower down payments or preferential rates, for armed forces and public servants.

Markup Rate & Tenure: Market competitive rates with standard tenures.

Best For: Serving and retired military personnel and government employees.

✅ Pros and ❌ Cons

✅ Excellent, tailored terms for its target audience.

✅ Efficient service for eligible customers.

✅ Strong relationship-based banking.

❌ Not the best option for those outside its core segment.

❌ Limited promotional offers for the general public.

4.7 Faysal Bank – Best Bank for Car Financing in Pakistan for Islamic Options

After its full conversion to an Islamic bank, Faysal Bank offers compelling Shariah-compliant auto finance products that give Meezan Bank a run for its money.

Overview: Faysal Islamic Auto Finance is based on the Diminishing Musharakah and Ijarah models.

Features: They offer flexible installment plans and have a growing network. Their conversion to a full-fledged Islamic bank has increased customer trust in their products.

Markup Rate & Tenure: They offer very competitive rates, around 13.5%, with tenures up to 7 years.

Best For: Customers looking for a strong, purely Islamic alternative to conventional banks.

✅ Pros and ❌ Cons

✅ 100% Shariah-compliant operations.

✅ Competitive profit rates.

✅ Good customer service.

❌ Brand recognition is still growing compared to Meezan.

❌ Network is not as extensive as some larger banks.

4.8 JS Bank – Best Bank for Car Financing in Pakistan for Custom Plans

JS Bank has positioned itself as an innovative player, often creating niche products for specific customer segments.

Overview: JS CarAamad focuses on providing tailored solutions.

Features: They offer unique packages for new graduates, small business owners, and women, sometimes with features like lower initial payments.

Markup Rate & Tenure: Rates are market-based, but the flexibility in structure is their key selling point.

Best For: Young graduates, entrepreneurs, and those who need a non-standard financing plan.

✅ Pros and ❌ Cons

✅ Highly customizable plans.

✅ Focus on niche segments.

✅ Innovative digital tools.

❌ Smaller branch network than big players.

❌ Not as widely recognized for auto finance.

4.9 Dubai Islamic Bank – Best Bank for Car Financing in Pakistan for Faith-Based Customers

DIB Pakistan brings the global expertise of its parent company to offer reliable and transparent Islamic auto finance.

Overview: Their Islamic auto finance product is structured with a clear and transparent rental agreement.

Features: They emphasize full Shariah compliance and clarity in all transactions, with no hidden charges.

Markup Rate & Tenure: Competitive Islamic banking rates with standard tenures.

Best For: Customers who value the global DIB brand and want a straightforward Islamic financing product.

✅ Pros and ❌ Cons

✅ Strong international Islamic banking pedigree.

✅ Transparent pricing.

✅ Good customer service.

❌ Relatively smaller market share in Pakistan.

❌ Fewer brand partnerships than larger banks.

4.10 Allied Bank – Best Bank for Car Financing in Pakistan for Corporate Customers

Allied Bank (ABL) has developed strong corporate solutions, making it a great choice for businesses and their employees.

Overview: ABL Car Finance includes special programs for corporate fleets and employee car financing schemes.

Features: They partner with companies to offer their employees car financing at preferential rates as a part of their benefits package.

Markup Rate & Tenure: Offer corporate-discounted rates.

Best For: Businesses looking to finance fleets and corporate employees availing company-offered car financing schemes.

✅ Pros and ❌ Cons

✅ Best-in-class corporate and fleet solutions.

✅ Attractive rates for employees of partner companies.

✅ Stable and reliable bank.

❌ Retail offerings for individuals may be less competitive.

❌ Less focus on digital innovation.

Comparison Table: Best Bank for Car Financing in Pakistan

Note: The following data is indicative for 2025. Markup rates are dynamic and must be verified directly from the official bank websites before making any decision.

| Bank Name | Indicative Markup Rate (p.a.) | Maximum Tenure | Minimum Salary (Approx.) | Processing Time | Financing Type |

|---|---|---|---|---|---|

| Meezan Bank | ~13% | 7 Years | PKR 30,000 | 5–7 Days | Islamic (Ijarah) |

| Bank Alfalah | ~14% | 7 Years | PKR 35,000 | 3–5 Days | Conventional |

| HBL | ~15% | 7 Years | PKR 40,000 | 7–10 Days | Conventional |

| MCB Bank | ~14.5% | 7 Years | PKR 30,000 | 5–7 Days | Conventional |

| Faysal Bank | ~13.5% | 7 Years | PKR 35,000 | 6–8 Days | Islamic |

| UBL | ~14% | 7 Years | PKR 35,000 | 7–10 Days | Conventional |

| Askari Bank | ~14.5% | 7 Years | PKR 35,000 | 7–10 Days | Conventional |

| JS Bank | ~15% | 7 Years | PKR 30,000 | 5–7 Days | Conventional |

| Dubai Islamic Bank | ~14% | 7 Years | PKR 40,000 | 7–10 Days | Islamic |

| Allied Bank | ~14.5% | 7 Years | PKR 40,000 | 7–10 Days | Conventional |

Tips to Get the Best Deal from the Best Bank for Car Financing in Pakistan

A little strategy can save you a lot of money.

- Maintain a Good Credit Score: Check your credit report from the Credit Information Bureau (CIB) of SBP. A high score makes you a low-risk customer and can help you negotiate a better rate.

- Increase Down Payment: As discussed, a larger down payment is the most effective way to reduce your monthly financial pressure and the total cost of the loan.

- Compare Multiple Banks: Don’t settle for the first offer you get. Get quotes from at least three different banks to leverage a better deal.

- Check for Hidden Charges: Scrutinize the financing agreement for processing fees, early settlement penalties, and late payment charges.

- Negotiate the Insurance Plan: Often, the bank’s tied-in insurance can be expensive. Ask if you can procure your own insurance from a provider of your choice (while meeting the bank’s coverage requirements) to potentially save money.

Best Bank for Car Financing in Pakistan – Islamic vs Conventional Options

The choice between Islamic and conventional financing is fundamental for many Pakistanis.

Islamic Car Financing operates on asset-backed transactions. The bank buys the car and leases or sells it to you. There is no concept of interest; instead, there is a transparently disclosed profit margin (in Murabaha) or a rental fee (in Ijarah). This structure is considered more ethical and transparent by its adherents, as all costs are laid out upfront.

Conventional Car Financing is a straightforward interest-based loan. The bank lends you money, and you pay back the principal with interest calculated over the tenure.

Why the Preference? Many Pakistanis, for religious reasons, are increasingly opting for Islamic banking. Banks like Meezan and Faysal have seen massive growth as a result. However, conventional banks often counter with faster processes and extensive dealer networks.

| Type | Pros ✅ | Cons ❌ |

|---|---|---|

| Islamic Financing | – Shariah-compliant and interest-free (no Riba) – Transparent and ethical profit-based model – No hidden or compounding interest | – Slightly less flexible due to Shariah structure – Processing may take longer compared to conventional banks |

| Conventional Financing | – Usually faster approval and simpler process – Widely available and well-integrated with car dealers – Offers promotional deals and lower initial costs | – Involves Riba (interest), prohibited in Islam – May include hidden charges or less transparent pricing |

Final Verdict: Which Is the Best Bank for Car Financing in Pakistan?

After a detailed analysis, it’s clear that the crown for the best bank for car financing in Pakistan is shared based on customer profiles and priorities.

For Low Markup & Islamic Compliance: Meezan Bank and Faysal Bank are the undisputed leaders, offering competitive, Shariah-compliant solutions.

For Quickest Approval & Digital Experience: Bank Alfalah stands out with its efficient, tech-driven process.

For Used Car Flexibility: UBL offers the most robust and flexible financing options for pre-owned vehicles.

For Salaried Individuals & Existing Customers: MCB Bank provides excellent value, especially if you already bank with them.

For Corporate & Fleet Deals: Allied Bank has specialized products that are hard to beat for businesses.

Your final decision should be a balance of the markup rate, the bank’s reputation, and the quality of service you expect. We strongly encourage you to visit the official websites of your shortlisted banks, use their online calculators, and even visit a branch to get the most current offer. Visit the official websites to apply today.

FAQs: The Best Bank for Car Financing in Pakistan

Which is the best bank for car financing in Pakistan right now?

There is no single “best” bank for everyone. However, for low markup and Islamic financing, Meezan Bank is highly recommended. For fast approval, Bank Alfalah is a top choice. Your personal financial situation and preferences will determine the best fit for you.

What are the lowest markup rates offered by Pakistani banks in 2025?

As of 2025, the lowest markup rates are generally offered by Islamic banks. Meezan Bank and Faysal Bank are consistently offering rates between 13% to 14%, which are among the most competitive in the market. However, these rates are subject to change frequently.

Is Meezan Bank better than Bank Alfalah for car financing?

It depends on your priority. If Shariah compliance and a lower profit rate are your main concerns, then Meezan Bank is better. If you need your car financed as quickly as possible and prefer a seamless digital application, Bank Alfalah has a distinct advantage.

Can I get car financing in Pakistan without a salary slip?

Yes, but it is more challenging. Self-employed individuals can apply by submitting alternative documents like bank statements for the last 6-12 months, proof of business registration, and tax returns. The bank will assess your income stability based on these documents.

What documents are required to apply for car financing in Pakistan?

The standard documents required by almost all banks are:

Copy of your CNIC.

Two recent passport-sized photographs.

For salaried individuals: Last 3-6 months’ salary slips and a job certificate.

For self-employed individuals: Last 6 months’ bank statements and business proof.

One utility bill for proof of residence.

Conclusion

Navigating the world of car financing in Pakistan can seem daunting, but it is a journey worth taking for the freedom and convenience a car provides. The key is to be an informed consumer. The best bank for car financing in Pakistan is the one that aligns perfectly with your financial capacity, your timeline, and your ethical preferences. Whether you prioritize the religious compliance of Meezan Bank, the speed of Bank Alfalah, or the used-car expertise of UBL, there is a perfect option waiting for you.

Do your homework, compare the numbers beyond just the monthly installment, and read the fine print. Your dream car is within reach. Take the next step toward your dream car-choose wisely and drive smart.

You may also like: Govt loan schemes that can make you rich in 2026 - Try Now!

Inactivity reset active (10m)